Navigating Corporate Filings

Information Extraction via (Seek)Edgar

2026-04-23

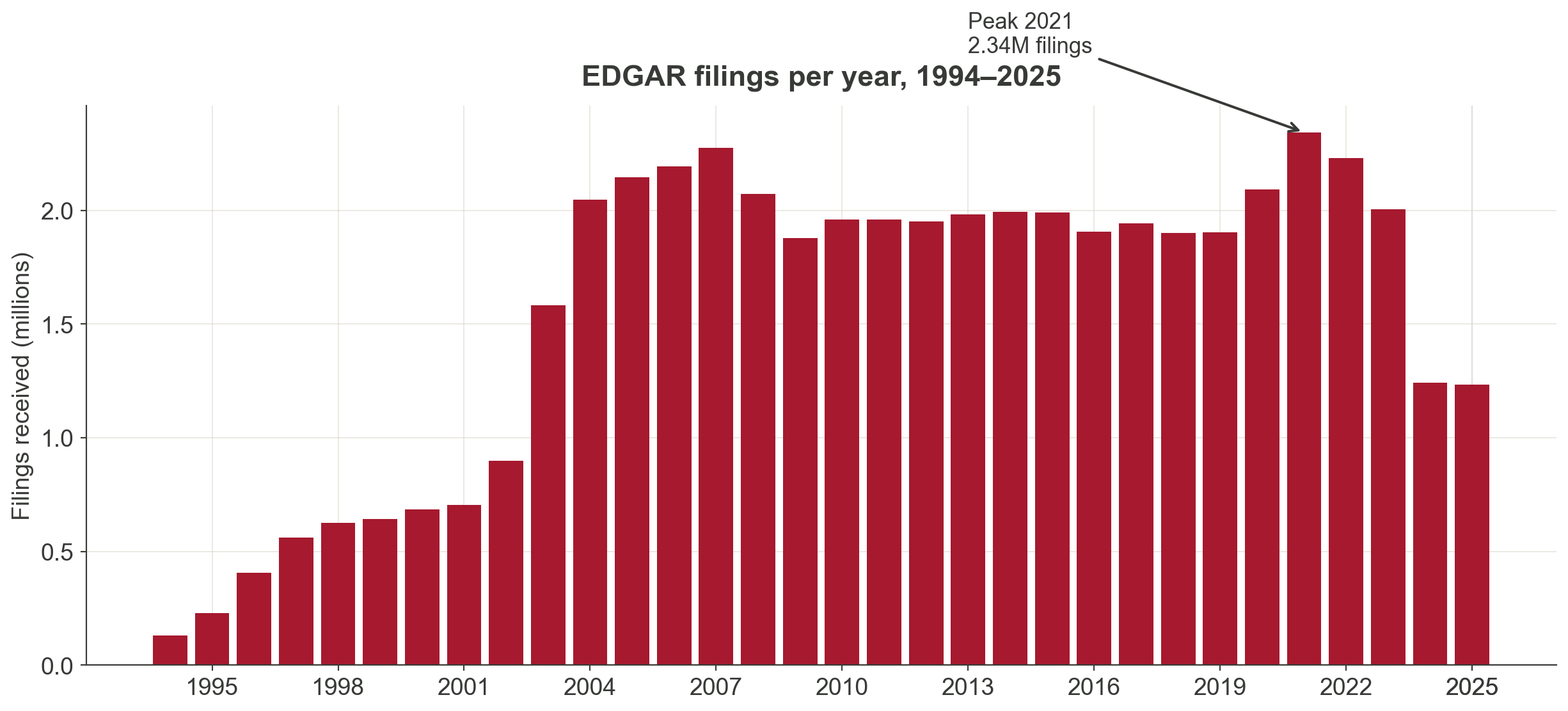

Three decades of growth

49.7M+

filings, 1994–2025

~2M / year

since 2004

~8,000 / day

new filings on a typical business day

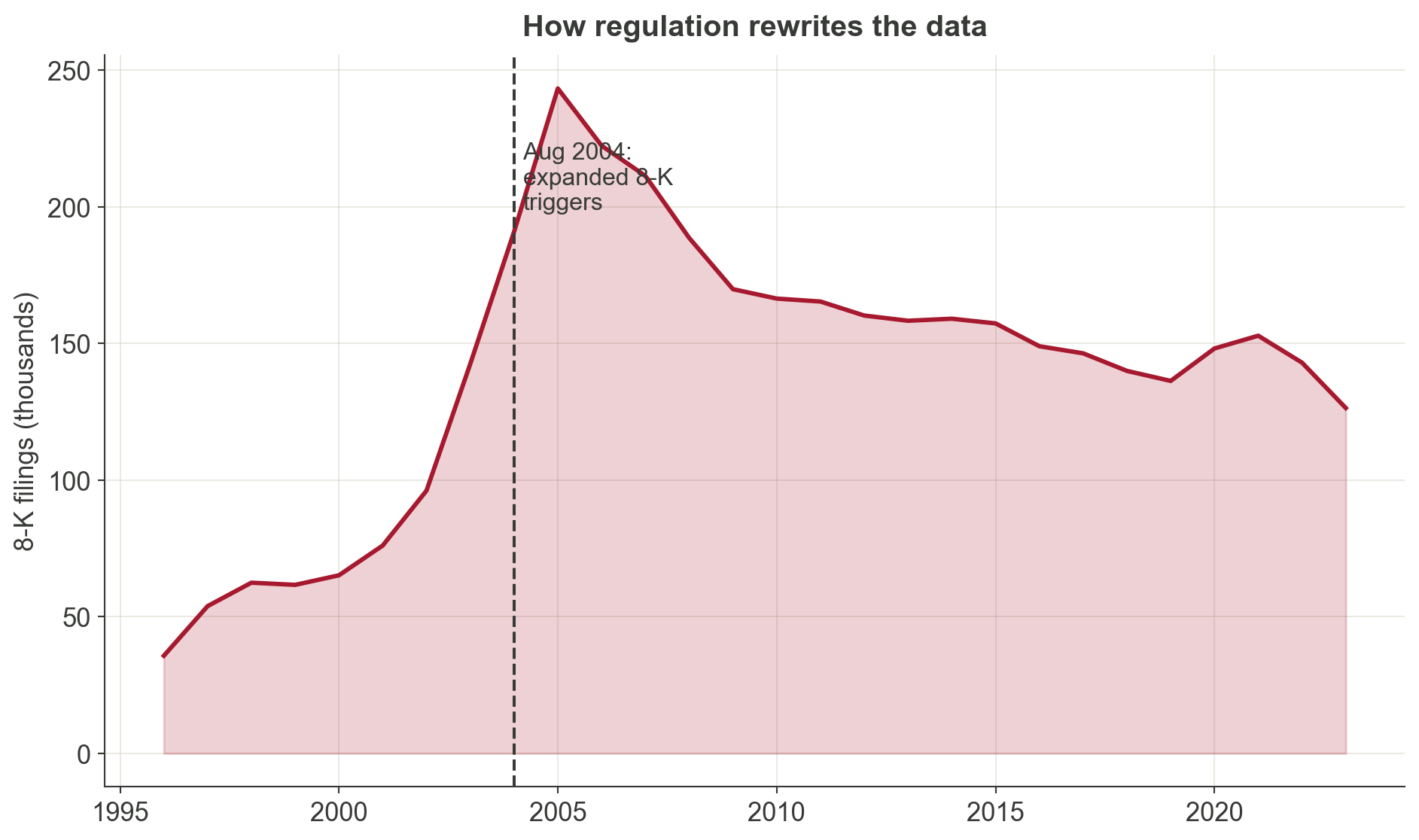

Regulation leaves fingerprints. The 2003–2004 step-up reflects expanded 8-K triggers and ownership-reporting rules.

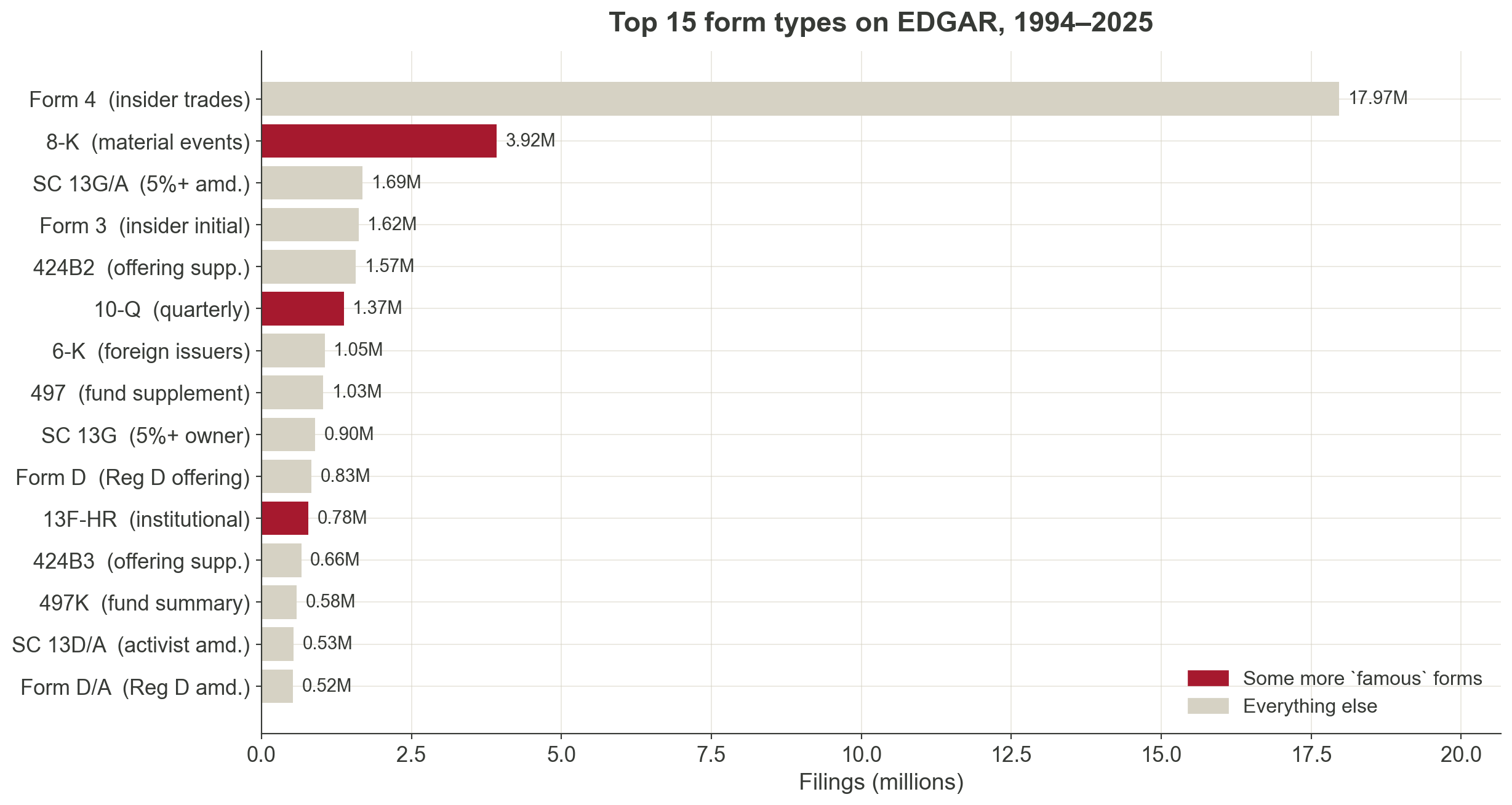

Top forms by filing count

The most-filed form you probably haven’t heard of

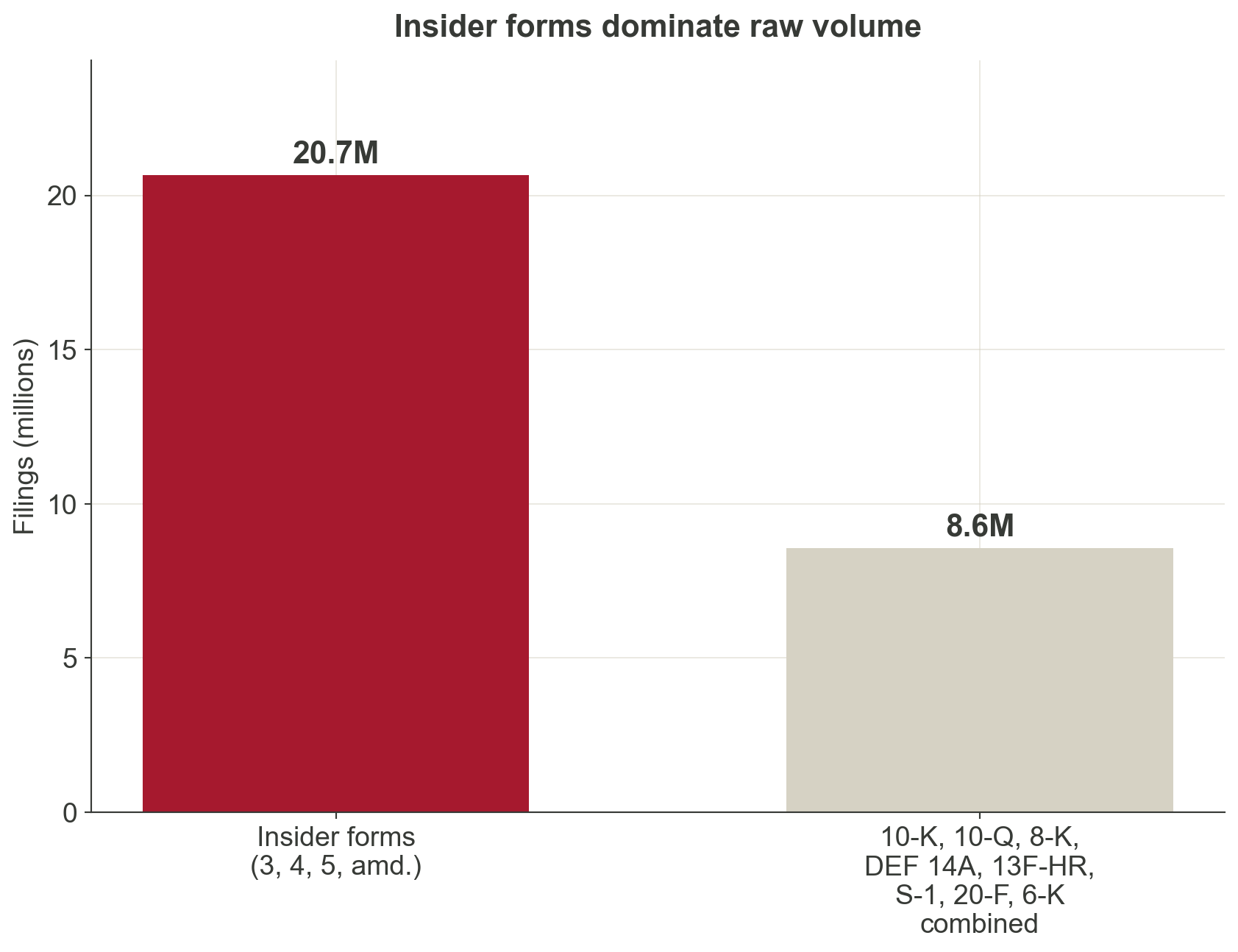

Form 4 is a one-page filing that an officer, director, or 10% shareholder submits within two business days of trading their company’s shares.

- 17.9 million Form 4 filings since 1994.

- More than 10-K, 10-Q, and 8-K combined.

- Each filing reveals who traded, how much, at what price, when.

Research idea

Do insiders sell systematically before negative news? Do director purchases signal board confidence? Form 4 gives you the raw material.

Who files the most? (not who you think)

Not Apple. Not Tesla. The most prolific filers are investment banks, asset managers, and their structured-product issuing vehicles submitting thousands of offering supplements and ownership reports. The “firm” in your data is not always the “firm” in your theory.

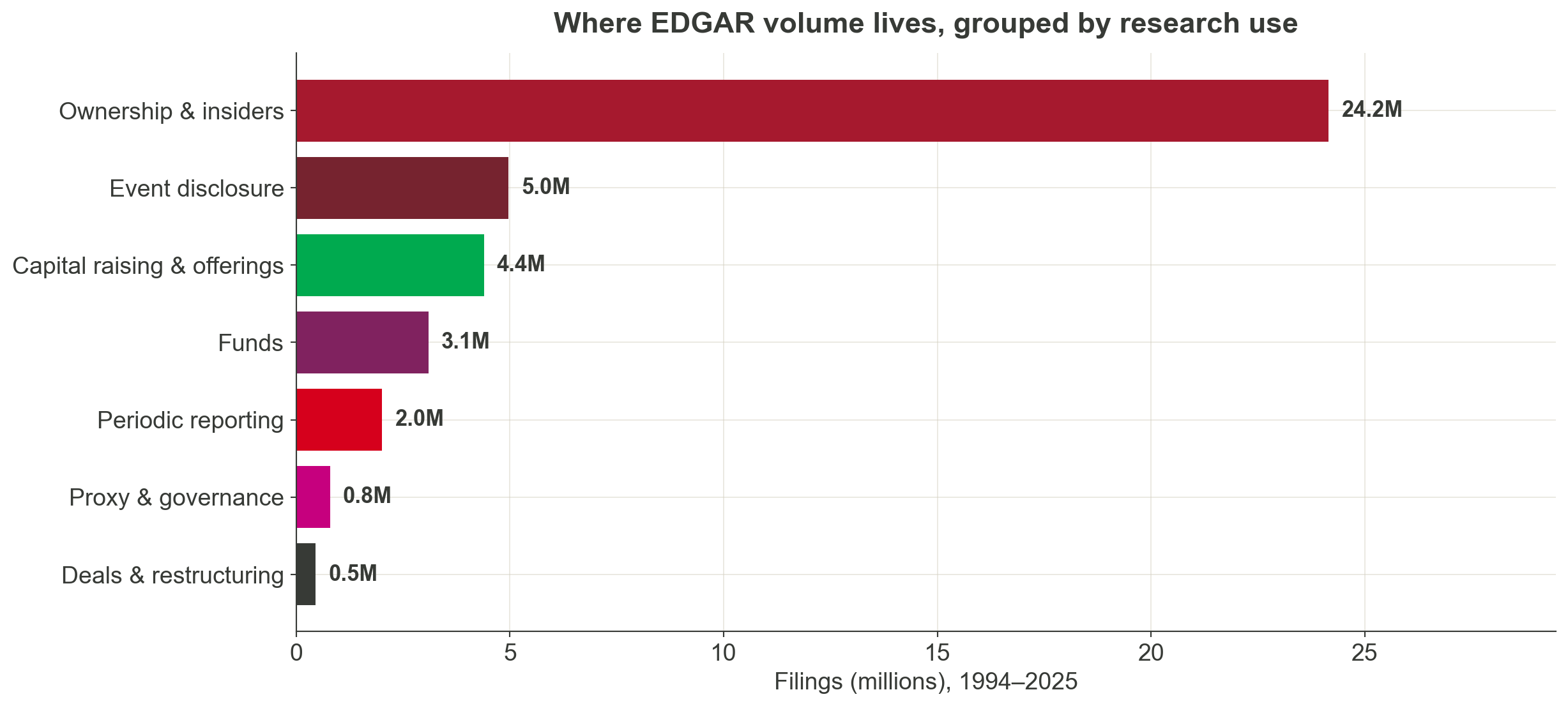

Filings grouped by research use

Periodic reports

The recurring narrative of the firm.

10-K (annual):

- Business description, risk factors, MD&A.

- Audited financial statements and footnotes.

- Segment and geographic discussion.

- Controls, legal proceedings, management certification.

10-Q (quarterly):

- Condensed financials and MD&A update.

- Updated risk factors and legal proceedings.

- Interim-period events between 10-Ks.

Things researchers have measured from 10-K / 10-Q:

- Cybersecurity and AI risk language.

- Customer concentration and supply-chain exposure.

- Climate disclosures and accounting estimates.

- Year-on-year and quarter-on-quarter text changes.

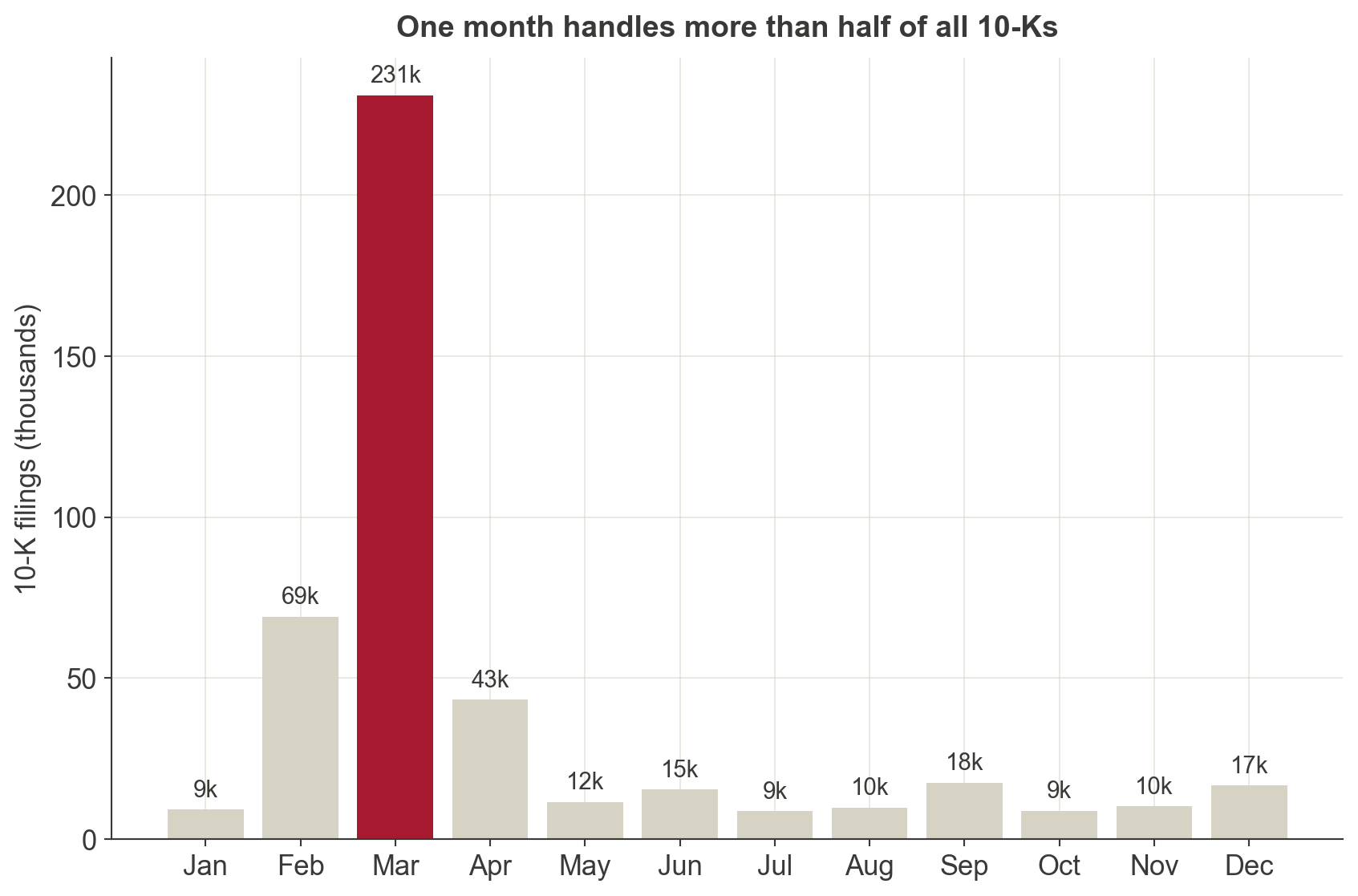

Most U.S. firms have a December fiscal year-end. Large filers must submit their 10-K within 60 days, others within 75–90 days. The calendar shapes the data.

Event-driven filings

When something material happens.

8-K can report:

- Material agreements, impairments, restatements.

- Leadership changes, auditor changes.

- Results announcements, financing events, acquisitions.

6-K transmits material information disclosed by foreign issuers abroad.

Research idea

Registration statements

Firms telling their story to investors.

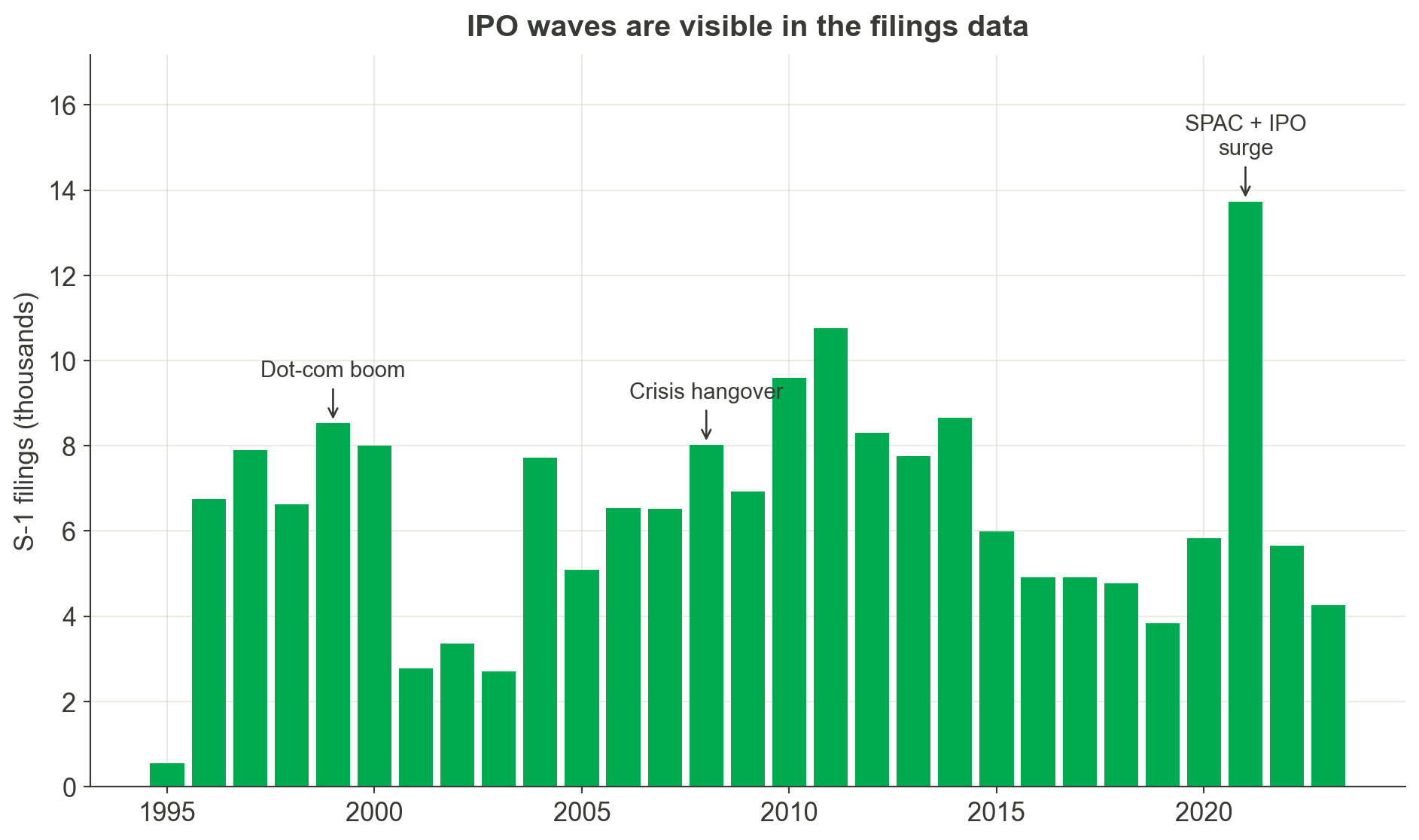

- S-1, F-1: IPOs and foreign issuers.

- S-3 and prospectuses: seasoned offerings.

Why this matters for research:

- Rich textual information exists before public trading history.

- Founder control, lock-ups, and risk narratives are disclosed here.

- Useful for entrepreneurship, innovation, and capital-market research.

Market history is written in these filings. Dot-com (1999–2000), the post-crisis freeze (2008–2009), and the 2021 SPAC / IPO wave all show up as bumps in the S-1 series.

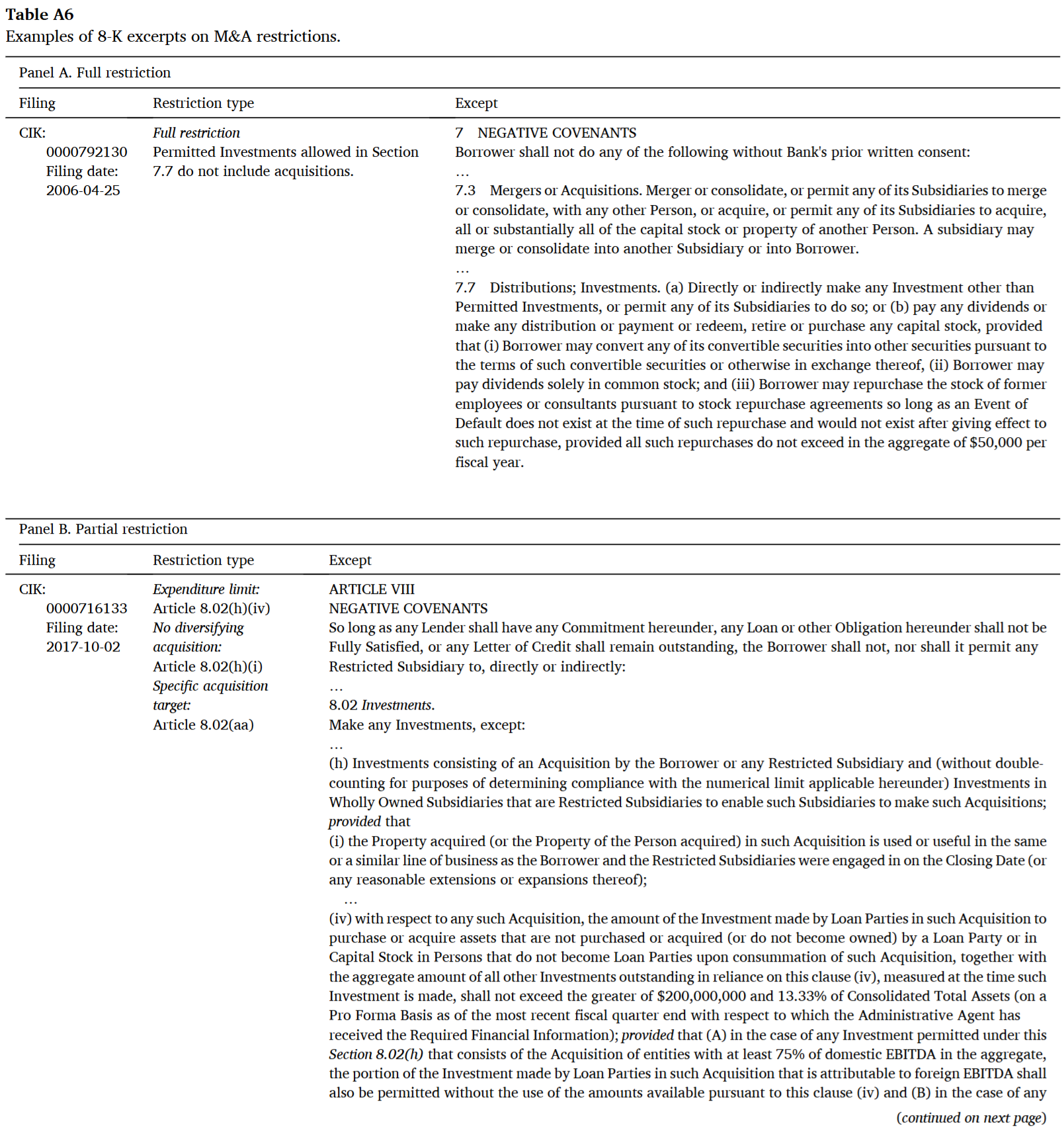

Case study: loan contracts in 8-K filings

- Gao et al. (2026) studies how lenders restrict borrower M&A through covenants in syndicated loan contracts.

- To examine the question, we need clause-level covenant data — the specific restrictions and exceptions that actually bind borrowers.

- But this is not available anywhere. DealScan, WRDS, and Compustat record deal pricing and financial covenants, not acquisition-restriction clauses.

- So we go to the raw filings: credit agreements are disclosed as EX-10 exhibits attached to 8-Ks, 10-Ks, and 10-Qs.

- We hand-collect the exhibits from EDGAR, code acquisition-restriction covenants, and link to DealScan and SDC M&A deals.1

- Contribution: prior work gave us a theory of lender screening and monitoring. We document the contractual mechanism — which clauses are written, when they bind, and how they change the M&A a borrower can pursue.2