AFIN8003 Week 9 - Liability and Liquidity Management

Banking and Financial Intermediation

Dr. Mingze Gao

Department of Applied Finance

2026-05-05

Liability and Liquidity Management

Cold open: 14 September 2007

Newcastle, Friday morning

Customers queued around the block outside Northern Rock branches.

It was the first run on a British bank since Overend, Gurney & Co. in 1866 — 141 years.

We’ll come back to why in a moment.

What killed Northern Rock?

It wasn’t bad loans. The mortgage book was performing.

It was the funding mix:

- ~75% of Northern Rock’s funding came from wholesale markets — securitisation, interbank lines, mortgage-backed securities.

- ~25% came from retail deposits.

When the asset-backed commercial paper (ABCP) market seized in August 2007, the bank could not roll its debt.

The Bank of England announced emergency liquidity assistance on the evening of 13 September. The news leaked. The next morning, the queues formed.

The lesson for this week

A bank’s liability mix is a liquidity-risk decision.

| Last week (Week 8) | This week (Week 9) |

|---|---|

| What is liquidity risk? | What’s the toolkit to manage it? |

| LCR, NSFR — measurement | Asset-side and liability-side instruments |

| The cost when it goes wrong | The cost of preventing it going wrong |

Throughout: every choice is a trade-off between cost and withdrawal risk. There is no free liquidity.

Roadmap

- Two sources of liquidity — stored and purchased.

- Asset-side toolkit — what counts as a liquid asset.

- The cash market and the RBA — how Australian banks settle.

- Liability-side toolkit — the deposit and wholesale ladder.

- The economics of a deposit — implicit and explicit interest.

- Other FIs and the 2025 regulatory update.

Two sources of liquidity

Where does the cash come from?

When a depositor walks in and asks for their money, the bank has two options.

Option 1. Sell something it already owns.

Option 2. Borrow new money from someone else.

That’s it. Every liquidity-management slide that follows is one of these two.

Stored liquidity, defined

Stored liquidity = selling or pledging liquid assets the bank already holds.

Examples:

- Cash.

- Reserves at the central bank (in Australia, the Exchange Settlement Account — defined later).

- Government bonds.

- High-grade securities.

The traditional approach. Used by all banks; relied on heavily by small banks.

Purchased liquidity, defined

Purchased liquidity = borrowing new funds in wholesale markets.

Examples:

- Overnight cash market between banks.

- Repurchase agreements (repos — defined shortly).

- Issuing wholesale certificates of deposit.

- Issuing bonds.

The modern approach. Relied on heavily by large banks. Northern Rock relied on it too heavily.

The fundamental trade-off

| Stored | Purchased | |

|---|---|---|

| Cost | Yield foregone on low-yielding assets | Funding spread above the cash rate |

| Risk in stress | Forced sale at fire-sale prices | Lenders disappear; cannot roll over |

| Effect on balance sheet | Shrinks (asset sold) | Stays the same size (new liability) |

Most modern banks use both. The mix is the strategy.

Asset-side toolkit

What makes an asset “liquid”?

An asset is liquid when it trades in a deep market.

Market depth

A market is deep if even large trades barely move the price.

Example: an Australian Government 10-year bond. You can sell A$500m in an afternoon at roughly the screen price.

Counter-example: a single residential mortgage. You can’t sell one. You have to securitise a portfolio of thousands.

The deeper the market, the lower the liquidation cost of the asset — and the more useful it is in a crisis.

The HQLA hierarchy (Week 8 recap)

HQLA = High-Quality Liquid Assets — the numerator of the LCR (Liquidity Coverage Ratio).

| Tier | Examples | Haircut |

|---|---|---|

| Level 1 | Cash, central-bank reserves, sovereign debt | 0% |

| Level 2A | High-grade corporate debt, covered bonds | 15% |

| Level 2B | Eligible RMBS, equities | 25–50% |

Level 2 combined cannot exceed 40% of total HQLA.

The haircut is the assumed loss-on-sale in stress.

The cost of holding HQLA

Every dollar of HQLA is a dollar not lent to a customer.

A simple example:

- Mortgage rate: 6%.

- Government bond yield: 4%.

- Holding HQLA instead of writing a mortgage costs the bank ~2% per year on that dollar.

This is why banks don’t just hold “lots of HQLA to be safe” — liquidity has a price.

The Exchange Settlement Account (ESA)

Every Australian bank has one account at the RBA: the Exchange Settlement Account.

- Used to settle obligations between banks at the end of each day.

- The balance in the ESA is called the bank’s ES balance.

- The RBA pays interest on the ES balance (currently the cash rate target minus 10 basis points).

Without an ESA, two banks cannot settle interbank payments. It is the operational core of the Australian payment system.

The cash market and the RBA

The cash market — price and quantity

The cash market is where banks lend and borrow ES balances, usually overnight.

Two variables matter:

- Price. The interest rate on these overnight loans is the cash rate.

- Quantity. The total ES balances banks hold at the RBA.

The RBA’s job is to keep the cash rate close to its target.

The cash rate target

The cash rate target is the RBA’s headline policy rate — the number that hits the news after every Board meeting.

Mortgage rates, business loan rates, deposit rates — all are anchored, directly or indirectly, to the cash rate.

The cash rate target is set by the RBA Board. The actual cash rate is determined by demand and supply in the cash market — and the RBA’s job is to align the two.

What is a repo?

Repo = repurchase agreement.

A repo is a sale today + an agreement to repurchase tomorrow:

- Bank A sells a bond to Bank B for $100 today.

- Bank A repurchases the same bond from Bank B for $100.05 tomorrow.

Economically, Bank A has borrowed $100 overnight at 5% (annualised), with the bond as collateral.

Repos dominate short-term funding because they’re secured — cheaper than unsecured lending.

The RBA’s pre-COVID world

Before March 2020:

- ES balances totalled around A$25 billion.

- The RBA actively managed the supply of ES balances each day, through repos with the banks.

- This kept the cash rate close to target.

This was a scarce reserves regime — banks competed for a limited pool of reserves.

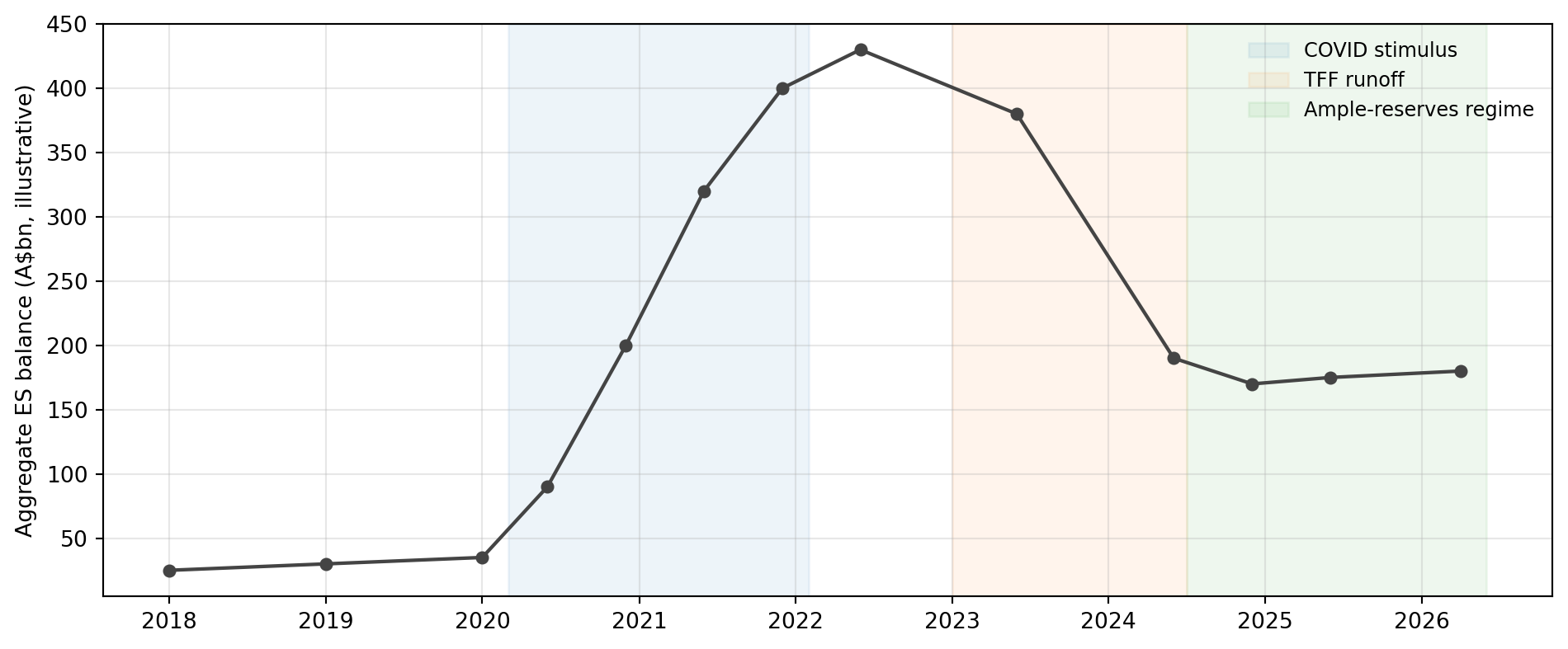

ES balances over time

Pre-COVID floor → COVID surge → post-TFF runoff → ample-reserves equilibrium.

Today: ample reserves

In March 2024 the RBA Board endorsed a permanent shift to an ample reserves framework.

The mechanics:

- Each week, the RBA runs a full-allotment repo auction.

- Banks bid for as many reserves as they want.

- The RBA charges the cash rate target plus 5 basis points.

- The RBA delivers all bids in full.

The RBA no longer controls the quantity of reserves — banks do. The RBA controls the price.

Other RBA facilities

Three smaller facilities round out the toolkit.

| Facility | What it does |

|---|---|

| Intra-day repo | Liquidity within a business day; reversed before close. |

| Overnight repo | Funds end-of-day liquidity needs. |

| Standing Facility | Penalty-rate overnight backstop if the ESA goes short. |

The standing facility exists for emergencies. Routine liquidity goes through the weekly OMO.

Two facilities that disappeared

Term Funding Facility (TFF) — 2020 to 2024

COVID-19 crisis tool. Banks could borrow up to 3 years at the cash rate target.

- Drawdown window closed 30 June 2021.

- Banks drew $188 billion at the peak — about 6% of all credit outstanding.

- All TFF funding fully matured by 30 June 2024.

Committed Liquidity Facility (CLF) — 2015 to 2023

A uniquely Australian fix. Basel III’s LCR requires HQLA. The Australian Government simply doesn’t issue enough debt for ADIs to hold sufficient Level 1 securities. The CLF was a paid line of credit from the RBA that counted as HQLA.

The post-COVID surge in Commonwealth bond issuance solved the underlying problem. APRA reduced the aggregate CLF from $140bn (Sep 2021) to zero on 1 January 2023.

Liability-side toolkit

Switching to the liability side

The goal of liability management:

Construct a portfolio of liabilities that is low cost and has low withdrawal risk.

The problem:

- Cheap funding tends to be flighty (demand deposits).

- Sticky funding tends to be expensive (term deposits, long bonds).

There is no free quadrant. Northern Rock learned this the hard way.

The cost vs. withdrawal-risk frontier

Cheap and sticky doesn’t exist. Banks pick a point on the frontier.

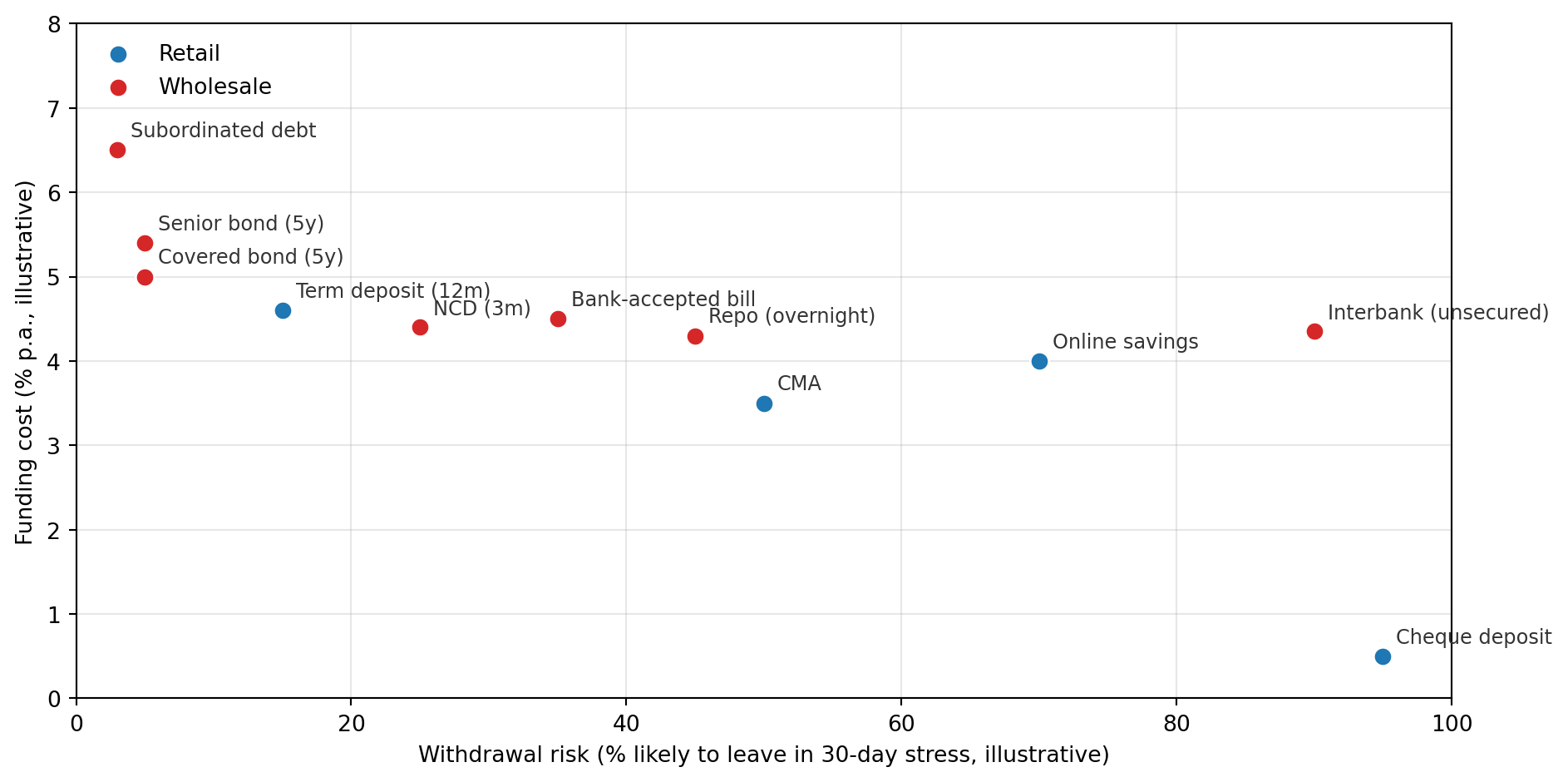

The deposit/wholesale ladder

We’ll walk through the major instruments in three groups.

- Deposit liabilities — cheque accounts, savings, CMAs, term deposits, NCDs.

- Wholesale liabilities — interbank, repos, bank bills, commercial paper.

- Long-term debt — covered bonds, subordinated debt, MTNs.

Each instrument sits somewhere on the frontier above. The order roughly matches retail to wholesale and short to long.

Deposit liabilities

Demand deposits

The cheque account, the everyday transaction account.

- Withdrawal risk: very high. Payable on demand, no notice.

- Cost (explicit interest): very low or zero.

- Used by: households and businesses for transactions.

Why are these so cheap for the bank?

The Regulation Q backstory

In the United States, demand deposits paid zero interest from 1933 to 2011.

Regulation Q (1933 Banking Act)

After the 1930s banking panics, U.S. regulators believed competition for deposits had pushed banks to take excessive risk.

Regulation Q prohibited U.S. banks from paying any interest on demand deposits. The prohibition lasted 78 years.

Section 627 of the Dodd–Frank Act repealed it on 21 July 2011. Banks are now permitted — but not required — to pay. Most still don’t.

Australia never had this prohibition. That’s why an Aussie online transaction account in 2026 can pay 4–5% while a Bank of America checking account pays ~0.01%.

Demand deposits aren’t really free

Even when explicit interest is zero, the deposit costs the bank real money:

- Branch staff, ATMs, online banking, fraud monitoring, 24/7 call centres.

- Cheque clearing.

- Card scheme fees.

Competition forces banks to partially absorb these costs and offer subsidised services. The depositor receives implicit interest — interest paid in services rather than cash.

The implicit interest rate

Define the implicit interest rate (IIR) on a demand-deposit account as:

\[ \text{IIR} = \dfrac{C - F}{B} \]

where, per account per year:

- \(C\) = bank’s management cost,

- \(F\) = fees earned by the bank,

- \(B\) = average annual balance.

If \(C > F\), the bank is subsidising the depositor. Implicit interest is positive.

If \(C < F\), the bank is taxing the depositor (fees exceed costs). Implicit interest is negative.

Calculator: implicit interest rate

Move \(C\), \(F\), and \(B\). The IIR updates live.

Code

viewof C = Inputs.range([0, 400], {value: 150, step: 5, label: "C ($/yr)"})

viewof F = Inputs.range([0, 400], {value: 100, step: 5, label: "F ($/yr)"})

viewof B = Inputs.range([200, 10000], {value: 1200, step: 50, label: "B ($)"})

iir = (C - F) / B

md`

IIR = ${(iir*100).toFixed(2)}%

${iir > 0

? "Bank subsidises the depositor — costs exceed fees."

: iir < 0

? "Bank taxes the depositor — fees exceed costs."

: "Costs and fees exactly net out."}

`The textbook example: \(C=\$150\), \(F=\$100\), \(B=\$1{,}200\). IIR ≈ 4.17%. The depositor “earns” 4.17% per year in subsidised services, even though the cash interest rate on the account is zero.

Gross interest = explicit + implicit

If an account also pays explicit interest above some minimum balance, the depositor’s total return is:

\[ G = \underbrace{r \cdot B \cdot \mathbb{1}\{B \ge M\}}_{\text{explicit}} \;+\; \underbrace{(c - f) \cdot n \cdot 12}_{\text{implicit}} \]

where:

- \(r\) = explicit interest rate (decimal, p.a.),

- \(B\) = average balance,

- \(M\) = minimum balance threshold to earn explicit interest,

- \(c\) = bank’s unit cost per transaction,

- \(f\) = fee charged per transaction,

- \(n\) = transactions per month.

The indicator \(\mathbb{1}\{B \ge M\}\) is 1 if the balance clears the threshold and 0 otherwise.

Calculator: gross interest

Code

viewof B2 = Inputs.range([0, 5000], {value: 1000, step: 50, label: "B ($)"})

viewof r = Inputs.range([0, 8], {value: 5, step: 0.05, label: "r (%)"})

viewof M = Inputs.range([0, 5000], {value: 500, step: 50, label: "M ($)"})

viewof c = Inputs.range([0, 0.5], {value: 0.15, step: 0.01, label: "c ($)"})

viewof f = Inputs.range([0, 0.5], {value: 0.10, step: 0.01, label: "f ($)"})

viewof n = Inputs.range([0, 200], {value: 50, step: 5, label: "n"})

explicit = B2 >= M ? B2 * (r/100) : 0

implicit = (c - f) * n * 12

gross = explicit + implicit

md`

Explicit = $${explicit.toFixed(2)}

Implicit = $${implicit.toFixed(2)}

Gross G = $${gross.toFixed(2)}

`Two things to try:

- Drop \(B\) below \(M\) — explicit interest collapses to zero.

- Drop \(f\) below \(c\) — implicit interest goes positive.

Savings accounts and CMAs

Two close cousins of the demand deposit, both with lower withdrawal risk.

Savings account

- Restrictions: limited monthly withdrawals, sometimes a notice period.

- Held for accumulation, not transactions.

- Pays explicit interest.

- Lower withdrawal risk than a cheque account.

Cash management account (CMA)

- High minimum balance (typically A$10,000+).

- Funds available on call; supports cheques, debit cards, transfers.

- Modest implicit interest, mitigated by transaction fees.

- Aimed at investors and treasurers parking cash between trades.

Term deposits and retail CDs

Fixed maturity, fixed rate, early withdrawal penalty.

- Withdrawal risk: very low — the penalty is the discipline device.

- Cost: high explicit interest. Banks pay a maturity premium.

- Used by yield-seeking retail savers.

For the bank, term deposits are the workhorse of long, sticky retail funding. The cost is a known number locked in for the term.

Negotiable certificates of deposit (NCDs)

A wholesale time deposit. Face value typically above ~A$100,000. Maturities from days to years.

The key word is negotiable: the holder can sell the NCD in the secondary market.

- Withdrawal risk for the bank: low. The bank doesn’t repay until maturity; the holder gets liquidity by selling.

- Cost: moderate. Market-driven, benefits from the issuer’s credit rating.

NCDs sit between retail term deposits and pure wholesale funding.

Non-deposit (wholesale) liabilities

Interbank funds

Short-term unsecured loans between banks, usually overnight.

- The price is the cash rate.

- Withdrawal risk for the borrowing bank: very high. The lender can refuse to roll over the next day.

- Cost: low to moderate — close to the cash rate.

This is the cheapest unsecured funding a bank can get. It’s also the first to disappear in a crisis.

Repurchase agreements (repos)

We met repos earlier as an RBA tool. Banks also use them with each other.

- The transaction is collateralised by securities.

- Cheaper than unsecured interbank lending — the lender bears almost no credit risk.

- Highly flexible: overnight, term, or open-ended.

Why secured beats unsecured

The repo lender holds your collateral. If you default, they sell it. So they don’t need to charge a credit risk premium.

In stress, secured markets often stay open while unsecured markets close. This is why every bank treasurer has a stack of repo-eligible collateral ready to go.

Bank-accepted bills and commercial paper

Two short-dated wholesale instruments.

Bank-accepted bill (BAB)

- A short-term bill of exchange that a bank guarantees (“accepts”).

- Sold to investors at a discount.

- Once the benchmark for the Australian short-rate (BBSW).

- Largely supplanted by NCDs and repos.

Commercial paper (CP)

- Short-term unsecured promissory notes.

- Issued by both banks and large corporates.

- Heavily used in U.S. money markets.

- September 2019 episode: U.S. repo rates spiked from ~2% to ~10% in a day when reserves drained — even “deep” wholesale markets can seize.

Covered bonds

A bond issued by the bank, backed by a ring-fenced pool of assets that stays on the bank’s balance sheet.

Why covered bonds are special

Bondholders have a dual claim:

- On the issuing bank, like any senior bond.

- On the cover pool (typically high-quality mortgages), if the bank fails.

Hence covered bonds are often rated AAA even when the issuer is rated AA−.

In Australia:

- Legalised by the Banking Amendment (Covered Bonds) Act 2011.

- Capped at 8% of the ADI’s domestic assets under APS 121.

- All Big 4 banks run active covered-bond programmes.

Subordinated debt and long-term borrowings

The bottom of the funding stack — long-dated, often callable, subordinated to depositors and senior creditors.

- Subordinated debt (Tier 2): counts toward regulatory capital. Expensive but stable.

- Medium-term notes (MTNs): a flexible programme for issuing bonds in various tenors and currencies.

- Senior unsecured bonds, long-term loans: the workhorse of long-term wholesale funding.

The most stable funding a bank can have, short of equity. Also the most expensive.

Other FIs and regulation

Liquidity management at non-DI FIs

The same trade-off, different instruments:

| FI type | Main funding | Distinct liquidity issue |

|---|---|---|

| Life insurer | Premiums, policy reserves | Mass policy surrenders |

| P–C insurer | Premiums, claims reserves | Catastrophe spike forces asset sales |

| Securities firm / IB | Repos, bank loans, short positions | Inventory financing during stress |

| Finance company | Commercial paper, long-term debt | CP rollover stress |

The unifying theme: short-term liabilities funding less-liquid assets, with rollover risk in the middle.

Regulation recap from Week 8

Australian liquidity rules sit under APRA’s Prudential Standard APS 210. Banks fall into one of two regimes:

| LCR ADI | MLH ADI | |

|---|---|---|

| Who | Big 4 + larger banks | Smaller ADIs |

| Core ratio | LCR ≥ 100% and NSFR ≥ 100% | Liquid assets ≥ 9% of liabilities |

| Liquid assets | HQLA (Level 1 + capped Level 2) | RBA-repo-eligible debt securities |

For depositors: the Financial Claims Scheme guarantees up to A$250,000 per account-holder per ADI, since 1 February 2012.

What’s new: APS 210, 1 July 2025

APRA finalised targeted changes in 2024 in response to the March 2023 banking turmoil.

Effective 1 July 2025:

- MLH ADIs must value their liquid assets at mark-to-market — no more amortised cost.

- All ADIs must be operationally ready to request Exceptional Liquidity Assistance (ELA) from the RBA.

- The headline 9% MLH minimum is unchanged.

Why it matters: an MLH ADI’s liquidity cushion will now visibly shrink when bond yields rise, rather than hide behind book values.

Wrap-up

Key takeaways

- Two sources of liquidity: stored (sell what you own) and purchased (borrow new). Banks use both.

- The cash market is a price (the cash rate) and a quantity (ES balances). The RBA’s 2024 pivot to ample reserves changes how the quantity is set.

- The CLF is gone. LCR ADIs now meet HQLA requirements with Commonwealth and semi-government bonds plus ES balances.

- Liabilities sit on a frontier between cost and withdrawal risk. There is no point that is both cheap and sticky.

- Implicit interest is real interest. A subsidised “free” account is genuinely paying you in services.

- APS 210 changes (1 July 2025) bring mark-to-market into the small-bank liquidity regime.

Suggested readings

- How RBA implements monetary policy

- RBA Exchange Settlement Account Policy

- RBA — The Future System for Monetary Policy Implementation (April 2024)

- RBA — The Committed Liquidity Facility: 2015–2022

- APRA — APS 210 Liquidity (Prudential Handbook)

- APRA — Targeted changes to ADI liquidity and capital standards (2024–2025)

- Covered bonds in Australia (RBA Bulletin)

References

AFIN8003 Banking and Financial Intermediation