AFIN8003 Week 8 - Liquidity Risk

Banking and Financial Intermediation

Dr. Mingze Gao

Department of Applied Finance

2026-04-28

Liquidity Risk

Why this week matters

Two bank deaths in 10 days — March 2023

| Silicon Valley Bank | Credit Suisse | |

|---|---|---|

| Run size | $42bn / day (≈25% of deposits) | CHF 110bn in days |

| Time to failure | 36 hours | One week |

| Trigger | $1.8bn AFS loss disclosure | Loss of confidence |

| Outcome | FDIC seizure | UBS takeover for CHF 3bn |

| Solvent on paper? | Yes | Yes |

Both banks died of thirst, not insolvency. A bank’s funding model is as much a risk as its loan book.

Roadmap

Two sides of the same risk

| Liability side | Asset side | |

|---|---|---|

| Trigger | Depositors / wholesale funders demand cash | Borrowers draw committed lines; investment portfolio loses value |

| Symptom | Net deposit drain | Forced asset sales |

| Cost | New funding at higher rates | Fire-sale loss on long-duration assets |

| Key concept | Distribution of net deposit drains; core deposits | Loan commitments; HQLA haircuts |

| March 2023 example | $42bn SVB run in one day | $1.8bn SVB AFS loss |

We focus on DIs — the institutions most exposed because they fund long-term assets with short-term, on-demand liabilities.

Sources of liquidity risk at DIs

Liability-side liquidity risk

- A DI’s balance sheet typically features a large amount of short-term liabilities funding relatively long-term assets.

- Short-term liabilities: demand deposits, other transaction accounts, etc.

- Long-term assets: mortgages, C&I loans, etc.

- Demand deposit accounts, money market deposit accounts (MMDAs), and other transaction accounts allow holders to demand immediate repayment of the face value in cash.

- For example, a DI with 20% of its liabilities in demand deposits, MMDAs, and other transaction accounts must be ready to liquidate assets to cover that amount on any banking day.

Scale of the maturity mismatch

For U.S. commercial banks, deposits typically make up 70–80% of total liabilities and capital, while cash assets are a small single-digit-to-low-teens share of total assets. The maturity mismatch is the business model — and the source of the risk.

Liability-side liquidity risk (cont’d)

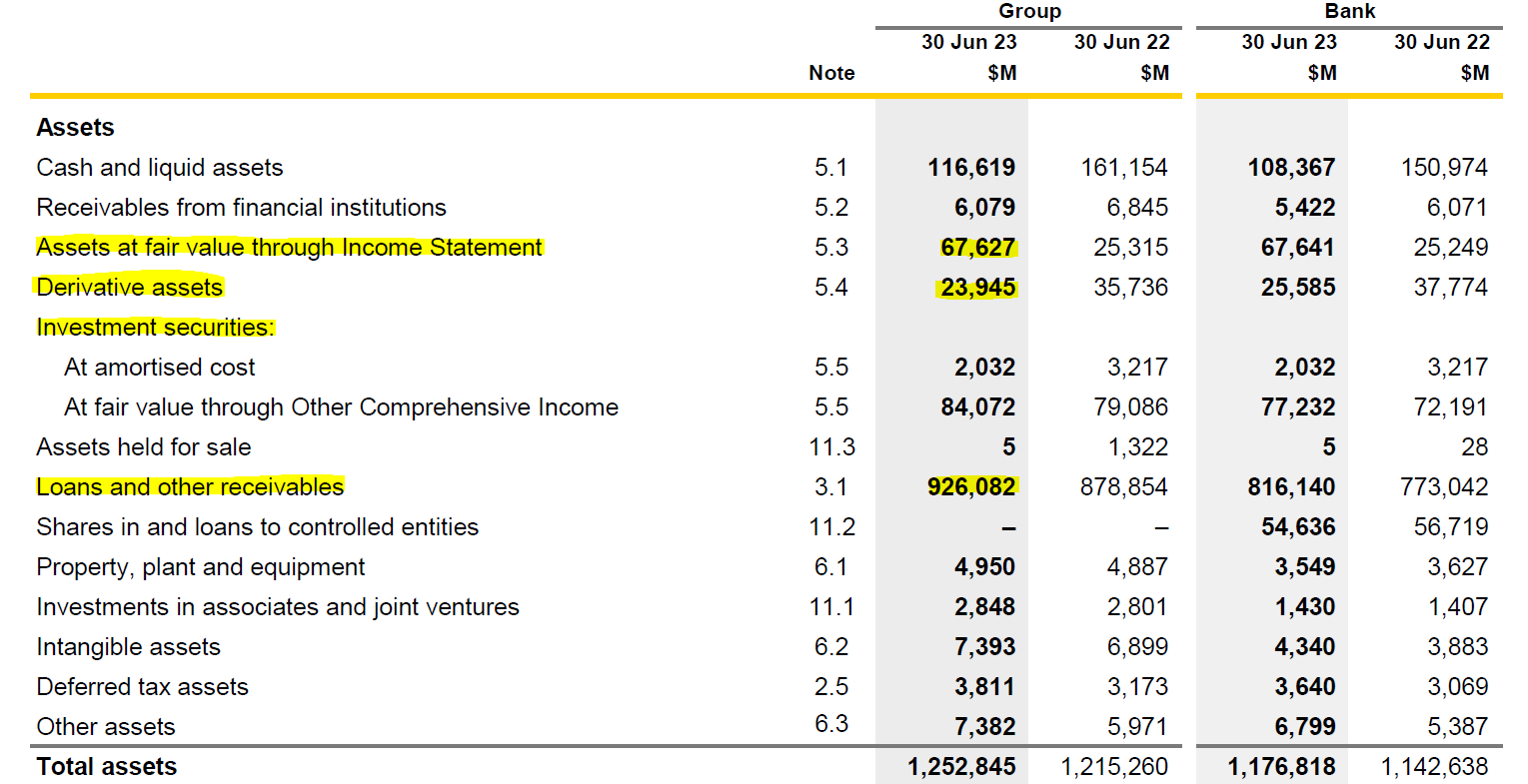

For CBA (FY2023), cash and liquid assets accounted for only 9.3% of total assets — the rest is largely loans and long-dated securities.

Figure 1: Excerpt of CBA’s FY2023 balance sheet — assets. Source: Commonwealth Bank of Australia 2023 Annual Report.

Liability-side liquidity risk (cont’d)

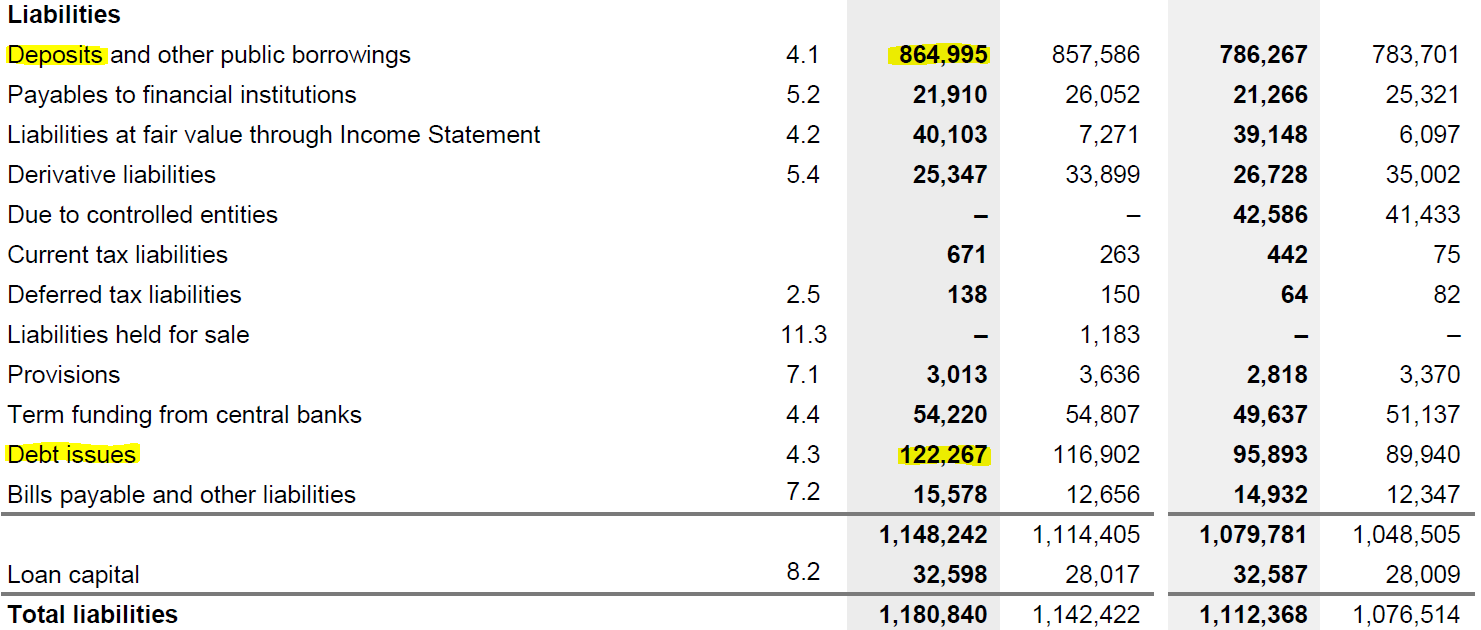

On the other side, CBA (FY2023) funded 73.25% of total liabilities with deposits and other public borrowings — most of it short-dated and on demand.

Figure 2: Excerpt of CBA’s FY2023 balance sheet — liabilities. Source: Commonwealth Bank of Australia 2023 Annual Report.

Liability-side liquidity risk (cont’d)

It’s not that bad.

- Normally, only a small proportion of its deposits will be withdrawn on any given day.

- Further, deposit withdrawals may in part be offset by the inflow of new deposits1 (and the DI’s income).

Most demand deposits are relatively “stable”, acting as consumer core deposits on a daily basis.

- Core deposits are those deposits that provide a DI with a long-term funding source.

The DI manager must monitor and predict the net deposit drains on any given normal banking day.

- Beyond predictable daily seasonality in deposit flows, other seasonal variations exist.

- Many of these seasonal variations are somewhat predictable.

- Retail DIs often experience above-average deposit outflows around the end of the year and in the summer (due to Christmas and the vacation season).

- Rural DIs may experience a deposit inflow–outflow cycle aligned with the local agricultural cycle.

- During the planting and growing season, deposits tend to fall.

- During the harvest season, deposits tend to rise as crops are sold.

Net deposit drains and how DIs manage them

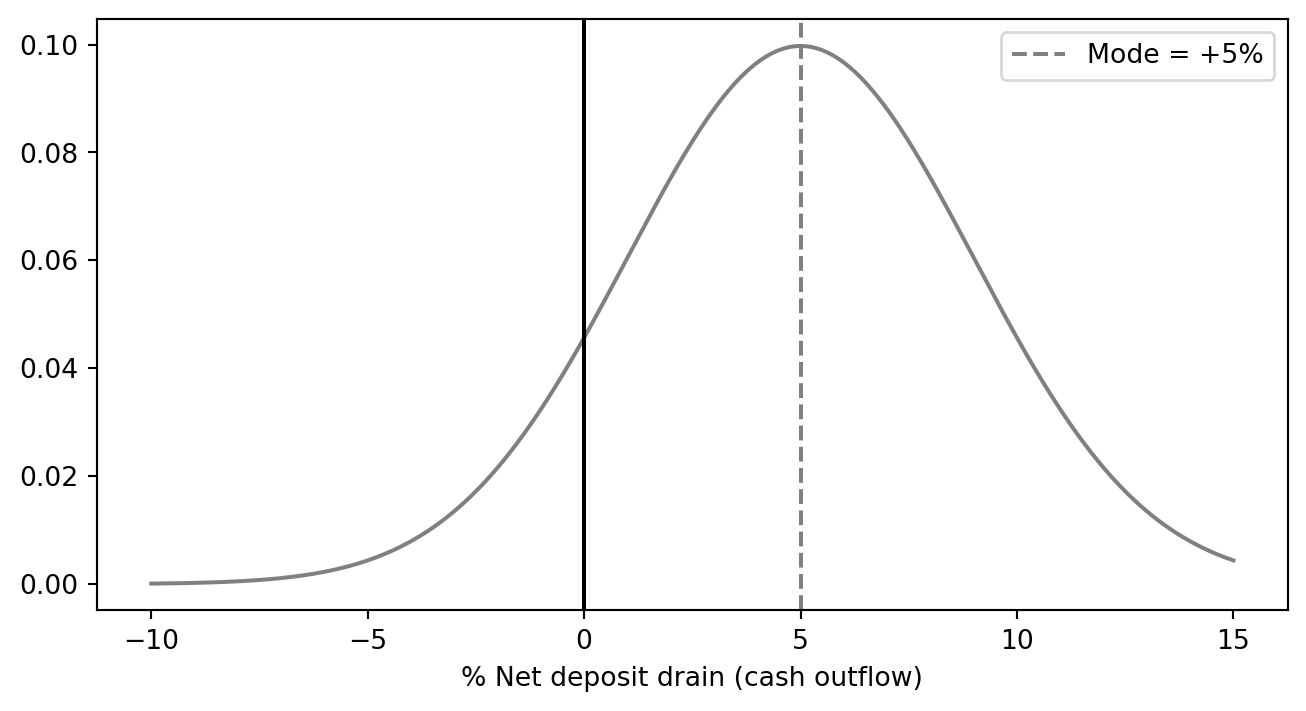

DI managers monitor the distribution of net deposit drains — the daily difference between withdrawals and inflows. Two stylised cases:

Code

import matplotlib.pyplot as plt

import numpy as np

x = np.linspace(-10, 15, 1000)

y = np.exp(-0.5 * ((x - 5) / 4)**2) / (4 * np.sqrt(2 * np.pi))

plt.figure(figsize=(8, 4))

plt.plot(x, y, color='gray')

plt.axvline(x=0, color='black', linestyle='-')

plt.axvline(x=5, color='gray', linestyle='--', label='Mode = +5%')

plt.xlabel("% Net deposit drain (cash outflow)")

plt.legend()

plt.show()

Mode at +5% ⇒ withdrawals routinely exceed inflows ⇒ liability side contracting.

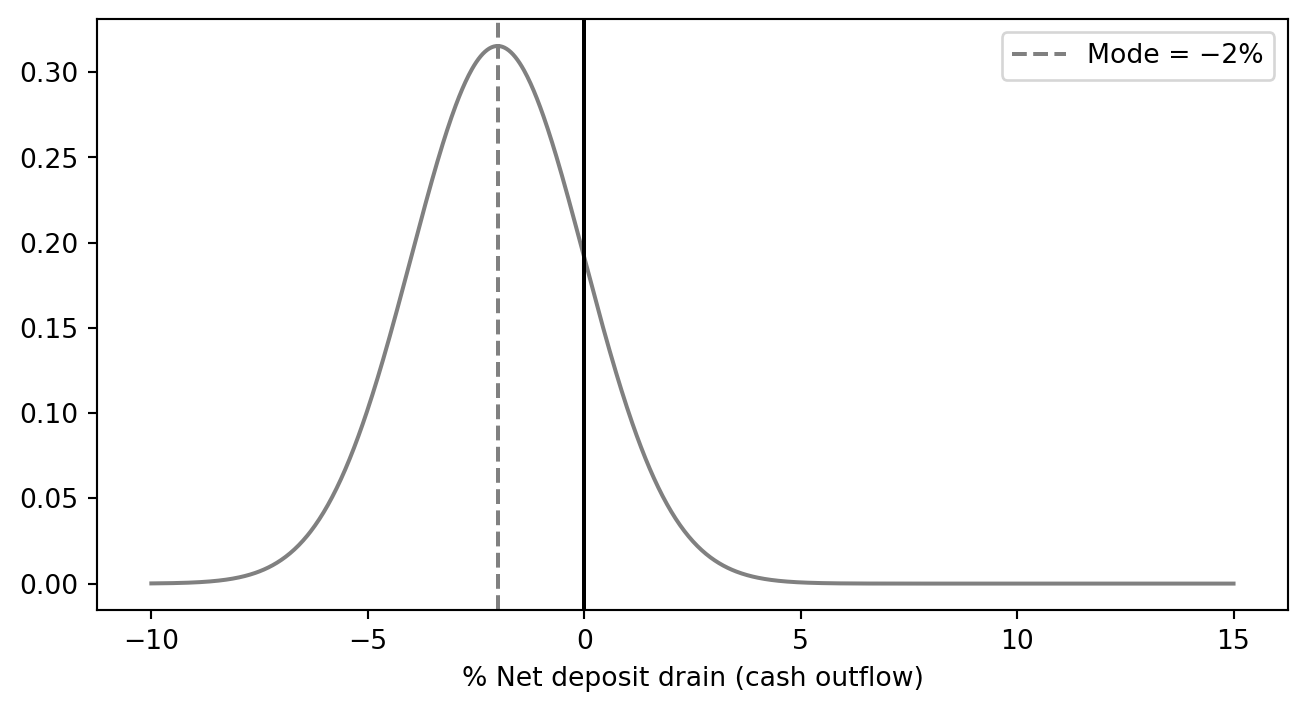

Code

import matplotlib.pyplot as plt

import numpy as np

x = np.linspace(-10, 15, 1000)

y = np.exp(-0.5 * ((x + 2) / 2 )**2) / (4 * np.sqrt(2 * 0.1 * np.pi))

plt.figure(figsize=(8, 4))

plt.plot(x, y, color='gray')

plt.axvline(x=0, color='black', linestyle='-')

plt.axvline(x=-2, color='gray', linestyle='--', label='Mode = −2%')

plt.xlabel("% Net deposit drain (cash outflow)")

plt.legend()

plt.show()

Mode at −2% ⇒ inflows exceed withdrawals ⇒ balance sheet expanding.

When a positive drain materialises, the DI plugs it via either purchased liquidity (wholesale borrowing) or stored liquidity (run down cash / HQLA). Traditionally DIs leaned on stored liquidity; today most rely on purchased liquidity — examined next.

Managing liquidity risk

Purchased vs. stored liquidity: side by side

A $5 deposit drain (deposits 70 → 65). Two ways to plug it:

(A) Purchased liquidity — borrow in wholesale markets (interbank, repo, CDs, notes/bonds).

| Before | After drain | After fix | |

|---|---|---|---|

| Assets | 100 | 100 | 100 |

| Deposits | 70 | 65 | 65 |

| Borrowed | 10 | 10 | 15 |

| Other liab. | 20 | 20 | 20 |

| Total | 100 | 95 | 100 |

✓ Balance sheet size preserved. ✗ Wholesale funding is costlier and flightier than deposits.

(B) Stored liquidity — run down cash and HQLA buffers.

| Before | After drain & fix | |

|---|---|---|

| Cash | 9 | 4 |

| Other assets | 91 | 91 |

| Deposits | 70 | 65 |

| Borrowed | 10 | 10 |

| Other liab. | 20 | 20 |

| Total | 100 | 95 |

✓ No new (expensive) funding. ✗ Balance sheet contracts; foregone return on the cash buffer.

Reserve requirements have largely faded

The U.S. Fed cut all reserve requirements to zero on 26 March 2020 and has not reinstated them; the RBA has never imposed a formal reserve ratio. Today, “stored liquidity” mostly means HQLA under the LCR, not regulatory cash reserves.

Asset-side liquidity risk: two channels

So far we have focused on liability-side drains. The asset side generates liquidity demand through two channels:

1. Loan-commitment drawdowns

Borrowers exercise pre-existing committed credit lines — the bank must fund the loan today, even though it priced the commitment yesterday.

COVID-19 dash for cash

In March 2020, U.S. corporates drew on credit lines at unprecedented speed. Acharya et al. (2024) link this drawdown channel directly to bank-stock underperformance during the pandemic.

2. Investment-portfolio losses

Rising rates → MTM losses on bond holdings. If the bank must sell to fund withdrawals, paper losses become realised losses, eating into equity.

SVB, March 2023

SVB sold its available-for-sale portfolio at an $1.8bn after-tax loss to raise cash for outflows. The disclosure itself triggered the run that killed the bank within 36 hours.

The mechanics of plugging an asset-side need (a $5 drawdown or $5 MTM hit) are the same as on the liability side: either purchase liquidity (more borrowing) or store liquidity (run down cash). The cost trade-offs are identical to the previous slide.

Asset-side liquidity risk: combined balance-sheet view

Loan-commitment exercise ($5 drawn)

| Before | Stored | Purchased | |

|---|---|---|---|

| Cash | 12 | 7 | 12 |

| Other assets | 138 | 143 | 143 |

| Deposits | 100 | 100 | 100 |

| Borrowed | 20 | 20 | 25 |

| Equity | 25 | 25 | 25 |

| Total | 150 | 150 | 155 |

Investment-portfolio MTM loss ($5)

| Before | Stored | Purchased | |

|---|---|---|---|

| Cash | 12 | 7 | 12 |

| Inv. port. | 50 | 50 | 50 |

| Other assets | 88 | 88 | 88 |

| Deposits | 100 | 100 | 105 |

| Borrowed | 20 | 20 | 20 |

| Equity | 20 | 20 | 20 |

| Total | 150 | 145 | 150 |

In both cases the stored route shrinks the balance sheet, and the purchased route preserves size at the cost of more wholesale funding.

Measuring liquidity risk

Measuring liquidity risk: from textbook to regulation

Liquidity-risk measurement has evolved through three layers. The first two (gap analysis, peer ratios) remain useful internal management tools; the Basel III LCR and NSFR are the binding regulatory standards.

| Layer | Measure | Question it answers | Status today |

|---|---|---|---|

| 1. Structural gap | Financing gap & financing requirement | How much wholesale funding do I need to plug the loan/deposit mismatch? | Internal ALM tool |

| 2. Peer benchmarking | Loan-to-deposit ratio, core deposits / assets, unused commitments / assets | How does my balance-sheet structure compare to peers and history? | Internal + supervisory monitoring |

| 3. Stress-based ratios | LCR (30-day), NSFR (1-year) | Can I survive 30 days of stress? Is my funding stable over 1 year? | Binding Basel III minima |

Financing gap in practice — the loan-to-deposit ratio

The financing gap is the textbook framing; the loan-to-deposit ratio (LDR) is the version banks and supervisors actually report.

\[ \text{Financing gap} = \text{Average loans} - \text{Average (core) deposits} \]

A positive gap must be filled by liquid assets sold or wholesale funding raised:

\[ \underbrace{\text{Financing gap}}_{\text{loans} - \text{deposits}} + \underbrace{\text{Liquid assets}}_{\text{stored}} = \underbrace{\text{Borrowed funds}}_{\text{purchased}} \]

Worked example — and the LDR view

A bank reports average loans of $25bn, deposits of $20bn, and liquid assets of $3bn.

- Financing gap = 25 − 20 = $5bn ⇒ requires $5bn of non-deposit funding.

- Of that, $3bn can come from liquid assets; the remaining $2bn must be borrowed.

- Equivalently, LDR = 25 / 20 = 125% — well above the ~70–80% typical for the Australian Big 4. The higher the LDR, the more the bank relies on wholesale funding (and, post-2008, the more attention APRA pays).

Other peer ratios worth watching

Common peer-comparison ratios:

- Loans to assets — overall illiquidity of the asset book.

- Core deposits to total assets — share of sticky, lower-cost funding.

- Unused loan commitments to assets — contingent draw-down exposure (this is the channel that bit banks in March 2020).

- Wholesale funding to total liabilities — how much short-term, flighty money the bank relies on.

The 2023 SVB autopsy turned all of these into headline metrics: SVB’s uninsured-deposit share was ~94%, and its HTM bond book was ~50% of assets — both extreme outliers among U.S. peers.

LCR — short-term resilience

Basel III: two ratios, two horizons

| LCR | NSFR | |

|---|---|---|

| Question | Survive 30 days of acute stress? | Funding stable over 1 year? |

| Horizon | 30 days | 1 year |

| Numerator | Stock of HQLA | Available stable funding (ASF) |

| Denominator | Net cash outflows in stress | Required stable funding (RSF) |

| Minimum | ≥ 100% | ≥ 100% |

| In force | Phased 1 Jan 2015 → fully 1 Jan 2019 | 1 Jan 2018 |

| Reporting | Monthly | Quarterly |

Did Basel III prevent SVB?

SVB sat just below the $250bn U.S. threshold — the strictest LCR/NSFR rules did not bind. The 2018 rollback of post-crisis rules for mid-sized U.S. banks (S.2155) is a recurring theme in post-mortems of March 2023.

Liquidity Coverage Ratio (LCR): the 30-day question

“If a severe liquidity stress hits today, can the bank survive for 30 days using only its own liquid assets?”

\[ \text{LCR} = \frac{\text{Stock of HQLA}}{\text{Total net cash outflows over the next 30 calendar days}} \ge 100\% \]

- Numerator — high-quality liquid assets the bank can sell, repo, or pledge in stress at little loss of value.

- Denominator — modelled net cash outflows under a prescribed stress scenario combining an idiosyncratic shock (e.g. a credit-rating downgrade) and a market-wide shock (e.g. GFC-style funding freeze).

- Reporting — at least monthly to supervisors, with daily computation capacity required.

Read the ratio as a survival horizon

LCR = 100% means the bank can survive exactly 30 days of the stress scenario on its own liquidity. LCR = 150% buys a bigger margin of safety; LCR < 100% means the bank fails the test and must rebuild its buffer.

Building the numerator: the HQLA stack

Two universal requirements for any asset to count as HQLA:

- Liquid in stress — convertible to cash at little loss of value and acceptable at the central-bank facility as collateral.

- Unencumbered — free of legal, regulatory, contractual, or other restrictions on the bank to liquidate, sell, transfer, or assign it.

| Tier | Examples | Haircut | Cap |

|---|---|---|---|

| Level 1 | Cash, central-bank reserves, sovereign/central-bank/PSE/multilateral debt (e.g. BIS, IMF, ECB, MDBs) | 0% | none |

| Level 2A | Other sovereign/PSE/MDB claims; high-grade corporate debt; covered bonds | 15% | combined Level 2 ≤ 40% of HQLA |

| Level 2B | RMBS (eligible) | 25% | of which Level 2B ≤ 15% of HQLA |

| Level 2B | Eligible corporate debt and equities | 50% | (subject to same Level 2B sub-cap) |

Why the haircuts matter — SVB again

SVB held a large portfolio of long-dated U.S. Treasuries and agency MBS — Level 1 / Level 2A on paper. The book was technically HQLA-eligible. The problem was that the bank classified much of it as held-to-maturity (HTM) at amortised cost: the unrealised losses didn’t show on the balance sheet, but they crystallised the moment SVB had to sell. The haircut framework prices in expected loss in stress; HTM accounting hid the loss until it was too late.

Building the denominator: net cash outflows

\[ \text{Net cash outflows} \,=\, \underbrace{\text{Out}}_{\text{outflows}} - \min\!\bigl(\underbrace{\text{In}}_{\text{inflows}},\ 0.75 \times \text{Out}\bigr) \]

- Outflows (\(\text{Out}\)) — every deposit, wholesale liability and contingent commitment, multiplied by a stressed run-off factor.

- Inflows (\(\text{In}\)) — contractual receipts within 30 days from performing assets.

- The 75% cap on inflows ensures the bank cannot rely entirely on incoming cash — it must hold a meaningful HQLA buffer regardless.

Run-off factors: pricing the flightiness of funding

The intuition: the more flighty the funding, the higher the assumed run-off.

| Liability type | Stressed run-off | Why |

|---|---|---|

| Stable retail deposits (insured, transactional) | 3–5% | Sticky; protected by deposit insurance |

| Less-stable retail deposits (e.g. brokered) | 10%+ | Less behavioural attachment |

| Operational corporate deposits | 25% | Tied to clearing/payments services |

| Non-operational unsecured wholesale (financial) | 100% | Will leave overnight in a crisis |

| Non-operational unsecured wholesale (corporate) | 40% | Slower, but still flighty |

| Undrawn committed credit lines (corporate) | 10% | Drawdowns spike in stress (cf. COVID-19) |

The hidden assumption: 30 days of that deposit base

LCR run-offs were calibrated to GFC-era deposit behaviour. The March 2023 SVB run exceeded the assumed retail/SME run-off in a single day, not 30. Post-2023 reviews by the Basel Committee, FRB, BoE, and APRA are explicitly considering whether run-off factors need to rise for highly digital, concentrated, or uninsured deposit bases.

Liquidity Coverage Ratio (LCR): example

Consider the following balance sheet (in million of dollars) of a bank. Calculate the bank’s LCR.

- Assume that the cash inflows over the next 30 days from the bank’s assets are $5 million.

| Assets | $ | Liquidity Level | Liabilities and Equity | $ | Run-Off Factor |

|---|---|---|---|---|---|

| Cash | 5 | Level 1 | Stable retail deposits | 95 | 3% |

| Deposits at the Fed | 15 | Level 1 | Less Stable retail deposits | 40 | 10 |

| Treasury securities | 100 | Level 1 | Unsecured wholesale funding from: | ||

| GNMA securities | 75 | Level 2A | - Stable small business deposits | 100 | 5 |

| Loans to A-rated corporations | 110 | Level 2A | - Less Stable small business deposits | 80 | 10 |

| Loans to B-rated corporations | 85 | Level 2B | - Nonfinancial corporates | 50 | 75 |

| Premises | 20 | Equity | 45 | ||

| Total | 410 | Total | 410 |

Liquidity Coverage Ratio (LCR): example (cont’d)

The LCR is calculated as follows:

First, calculate the amount of HQLA.

- Level 1 assets is \(5+15+100=120\) million

Before adjustment for caps,

- Level 2A assets is \((75+110)\times (1-15\%) = 157.25\) million1

- Level 2B assets is \(85\times (1-50\%)=42.5\) million2

However, Level 2 assets is capped at 40% of HQLA!

- Given that Level 1 assets is 120 million, which should account for at least \(1-40\%=60\%\) of HQLA.

- HQLA should be \(120/(1-40\%) = 200\) million, which means a maximum of \(200-120=80\) million Level 2 assets.

- The Level 2 assets after haircut is larger than the cap - they will not further increase HQLA.

Therefore, the HQLA is 200 million.

Liquidity Coverage Ratio (LCR): example (cont’d)

Next, calculate the total net cash outflows over next 30 days.

Cash outflows are:

- Stable retail deposits: \(95\times 0.03 = 2.85\)

- Less stable retail deposits: \(40\times 0.1 = 4\)

- Stable small business deposits: \(100\times 0.05 = 5\)

- Less stable small business deposits: \(80\times 0.1 =8\)

- Nonfinancial corporates: \(50\times 0.75 = 37.5\)

Therefore,

- Total cash outflows over next 30 days is 57.35 million.

- Total cash inflows over next 30 days is 5 million (assumed).

- Total net cash outflows over next 30 days is 57.35 million - min(5, 75% * 57.35) = 52.35 million.

Lastly, calculate LCR:

\[ \text{LCR} = \frac{\text{Stock of HQLAs}}{\text{Total net cash outflows over next 30 calendar days}} = \frac{200}{52.35} = 382.04\% \ge 100\% \]

NSFR — structural funding stability

Net Stable Funding Ratio (NSFR): the 1-year question

“Is the bank’s funding model structurally stable over a one-year horizon, or is it built on the kindness of overnight wholesale markets?”

\[ \text{NSFR} = \frac{\text{Available Stable Funding (ASF)}}{\text{Required Stable Funding (RSF)}} \ge 100\% \]

The LCR addresses acute stress (30 days); the NSFR addresses structural funding mismatch (1 year). Both must be ≥ 100% — they are complements, not substitutes.

Where it bites

The NSFR penalises banks that fund long-duration assets (long-term loans, illiquid securities) with short-term wholesale funding — exactly the funding model that blew up Northern Rock in 2007 and stressed European banks throughout the GFC.

NSFR: ASF and RSF factors

Available Stable Funding (ASF) weights liabilities + equity by how reliably they will stick around for a year. Required Stable Funding (RSF) weights assets by how illiquid / long-dated they are (i.e. how much stable funding they “need”).

ASF factors (selected)

| Funding source | ASF factor |

|---|---|

| Capital, liabilities with maturity > 1 year | 100% |

| “Stable” retail / SME deposits | 95% |

| “Less stable” retail / SME deposits | 90% |

| Non-financial corporate, sovereign, PSE funding < 1 year | 50% |

| Funding from financial institutions < 6 months | 0% |

Higher factor ⇒ “this funding is stable, count more of it.”

RSF factors (selected)

| Asset / OBS exposure | RSF factor |

|---|---|

| Cash, central-bank reserves | 0% |

| Level 1 HQLA | 5% |

| Level 2A HQLA | 15% |

| Performing residential mortgages (≤ 35% risk weight) | 65% |

| Other performing loans (residual maturity ≥ 1 year) | 85% |

| Non-performing loans, encumbered assets > 1 year | 100% |

| Undrawn committed facilities | 5% of notional |

Higher factor ⇒ “this asset locks up funding; you need more stable funding to hold it.”

Reading the formula

A bank holding lots of long-term mortgages (high RSF) funded mainly with overnight repos (low ASF) will fail the NSFR — exactly the funding-mismatch the rule is designed to discourage.

LCR & NSFR in practice — the Big 4

Liquidity risk of Australian banks (FY2023)

The figures below are drawn from the Big 4 banks’ FY2023 Pillar 3 disclosures. Workshop 8 will ask you to look up the latest figures from each bank’s most recent Pillar 3 report.

| CBA | NAB | ANZ | Westpac | |

|---|---|---|---|---|

| Cash Outflows | ||||

| Retail And Counterparties Deposits Outflow | 37,416 | 29,947 | 25,517 | 29,304 |

| Stable Deposits | 12,700 | 5,843 | 5,879 | 7,969 |

| Less Stable Deposits | 24,716 | 24,104 | 19,638 | 21,335 |

| Unsecured Wholesale Funding Outflow | 82,444 | 82,299 | 146,698 | 76,953 |

| Operational Deposit Outflow | 22,219 | 21,540 | 22,553 | 18,631 |

| Non Operational Deposits Outflow | 49,236 | 47,619 | 111,549 | 47,073 |

| Unsecured Debt Outflow | 10,989 | 13,140 | 12,596 | 11,249 |

| Secured Wholesale Funding Outflow | 6,839 | 10,701 | 5,405 | 3,891 |

| Additional Outflow Requirements | 26,186 | 38,693 | 70,639 | 30,463 |

| Derivative Expo And Other Collateral Requirement | 7,557 | 8,154 | 48,206 | 12,462 |

| Loss of Funding on Debt Products | 0 | 0 | 0 | 136 |

| Credit And Liquidity Facilities | 18,629 | 30,539 | 22,433 | 17,865 |

| Other Contractual Funding Obligation | 0 | 81 | 0 | 4,515 |

| Other Contingent Funding Obligation | 10,373 | 5,219 | 8,024 | 4,082 |

| Total Cash Outflow | 163,258 | 166,940 | 256,283 | 149,208 |

Liquidity risk of Australian banks (FY2023)

| CBA | NAB | ANZ | Westpac | |

|---|---|---|---|---|

| Cash Inflows | ||||

| Secured Lending | 2,328 | 3,898 | 1,549 | 0 |

| Inflows From Fully Performing Exposures | 9,520 | 11,788 | 17,190 | 5,020 |

| Other Cash Inflows | 6,753 | 1,589 | 36,016 | 7,988 |

| Total Cash Inflow | 18,601 | 17,275 | 54,755 | 13,008 |

Liquidity risk of Australian banks (FY2023)

| CBA | NAB | ANZ | Westpac | |

|---|---|---|---|---|

| Liquidity Coverage Ratio (LCR) | ||||

| Average High Quality Liquid Assets | 189,419 | 209,561 | 267,905 | 181,882 |

| Average Net Cash Outflows | 144,657 | 149,665 | 201,528 | 136,200 |

| Average Liquidity Coverage Ratio | 131.00 | 140.00 | 132.90 | 134.00 |

| Net Stable Funding Ratio (NSFR) | ||||

| Available Stable Funding | 860,999 | 646,508 | 625,285 | 707,893 |

| Required Stable Funding | 693,453 | 556,016 | 537,430 | 615,341 |

| Net Stable Funding Ratio | 124.00 | 116.00 | 116.35 | 115.00 |

What to notice

- All four banks sit comfortably above the 100% minimum for both LCR and NSFR.

- The range is narrow (LCR ~131–140%, NSFR ~115–124%) — this reflects APRA’s tight supervisory benchmarking, not coincidence.

- CBA’s NSFR (124%) is highest, consistent with its larger share of stable retail deposits.

- ANZ’s outflows ($256bn) are roughly 50% larger than the others, driven by a larger non-operational wholesale book.

Bank runs and safety nets

Liquidity planning

- Liquidity planning is crucial for managing liquidity risk and costs, helping with borrowing priorities and minimizing excess reserves.

- Components of a liquidity plan:

- Managerial responsibilities: Assign roles during a liquidity crisis and manage public disclosures.

- List of fund providers: Identify likely fund withdrawers and patterns, including sensitivity to funding composition changes.

- Withdrawal estimates: Assess potential deposit and fund withdrawals over different time horizons and identify funding sources.

- Internal limits and asset disposal: Set borrowing limits for subsidiaries and branches, determine acceptable risk premiums, and sequence asset disposals.

- The plan involves key departments like the money desk and Treasury for daily liability funding.

Liquidity risk, unexpected deposit drains, and bank runs

Major liquidity problems arise when deposit drains are abnormally large and unexpected, for reasons including:

- Concerns about a DI’s solvency relative to its peers.

- Failure of a related DI — the contagion effect.

- Sudden changes in investor preferences for holding non-bank financial assets (e.g. T-bills, money-market funds) over deposits — particularly when those alternatives offer materially higher yields.

In these cases, unexpected deposit drains can trigger a bank run that eventually forces the bank into insolvency. In the worst case, a bank panic spreads — a systemic, contagious run across the banking industry.

The 2023 run was different

Classic bank runs (think 1930s) propagated by word of mouth and physical queues. The March 2023 SVB run propagated by Slack, Twitter/X, and WhatsApp — and depositors moved money out of mobile apps in seconds, not hours. Regulators are now actively rethinking how fast LCR-style buffers can really last when the run velocity is digital.

Bank runs, the discount window, and deposit insurance

The two major liquidity risk insulation devices are deposit insurance and the discount window (or its central-bank equivalent).

- Deposit insurance — a public guarantee on insured deposits up to a per-depositor cap (US: FDIC; Australia: FCS).

- Discount window / lender-of-last-resort facilities — short-term central-bank lending against eligible collateral, at the “discount rate.”

- In the week ending 15 March 2023, U.S. banks drew $152.85 billion from the Federal Reserve’s discount window — a new record, eclipsing the $111 billion peak of the 2008 GFC.

- In Switzerland the same week, the SNB pledged CHF 50 billion of liquidity to Credit Suisse; when that was insufficient, the eventual support package totalled CHF 250 billion.

- In response to SVB, the Fed also launched the Bank Term Funding Program (BTFP), lending against high-quality securities valued at par (no haircut) — an unusually generous LOLR design.

Moral hazard

Insulation is not free. Insured deposits and easy LOLR access can encourage DIs to take more liquidity risk: hold riskier loans, fewer HQLA, more flighty wholesale funding. This is precisely why the Basel III LCR/NSFR rules exist — to put a regulatory floor under the liquidity buffer that protection might otherwise erode.

Liquidity regulation and depositor protection

Liquidity regulation in Australia

- In Australia, liquidity requirements are set by APRA.

- Prudential Standard APS 210 — Liquidity aims to ensure that an ADI has sufficient liquidity to meet obligations as they fall due.

APRA classifies each ADI as either:

- an LCR ADI (subject to the Basel III LCR, effective from 1 January 2015), or

- an MLH ADI (subject to the Minimum Liquidity Holdings regime, effective from 1 January 2014).

What changed in 2025

APRA finalised targeted changes to APS 210 in 2024 in response to the March 2023 banking turmoil. From 1 July 2025, MLH ADIs must adjust the value of their liquid assets regularly for mark-to-market movements (no more carrying at amortised cost — exactly the issue at SVB). All ADIs must also be operationally ready to provide key information when requesting Exceptional Liquidity Assistance (ELA) from the RBA. The headline 9% MLH minimum is unchanged.

LCR ADI vs. MLH ADI

APRA splits ADIs into two regulatory tracks under APS 210:

| Feature | LCR ADI | MLH ADI |

|---|---|---|

| Who | Larger / internationally active banks (the Big 4 and other significant ADIs) | Smaller ADIs (e.g. mutual banks, building societies, smaller credit unions) |

| Core requirement | Basel III LCR ≥ 100% and NSFR ≥ 100% | Liquid assets ≥ 9% of liabilities |

| Liquid asset definition | HQLA (Level 1 + capped Level 2, with haircuts) | RBA-repo-eligible, unsubordinated debt securities |

| Stress testing | Regular scenario analysis (at minimum: LCR scenario + “going concern”) | Operational capacity to liquidate liquid assets within 2 business days; trigger ratio set above 9% |

| Effective from | 1 January 2015 (LCR), 1 January 2018 (NSFR) | 1 January 2014 |

In short: LCR ADIs run the full Basel III stack; MLH ADIs run a simpler ratio-based regime scaled to their size and complexity.

Depositor protection

- Deposit insurance is a public mechanism designed to insulate depositors — and, indirectly, DIs — from liquidity crises.

- In the U.S., the Federal Deposit Insurance Corporation (FDIC) was created in 1933 in the wake of the Great Depression banking panics. The standard deposit insurance limit is $250,000 per depositor, per insured bank, per ownership category (raised from $100,000 in 2008).

- Most major economies now operate an explicit deposit insurance scheme.

- In October 2008, in response to the GFC, Australia introduced the Financial Claims Scheme (FCS) alongside a temporary wholesale funding guarantee.

- The FCS initially guaranteed deposit balances up to $1 million per depositor per institution.

- The permanent cap of $250,000 per account-holder per ADI has been in place since 1 February 2012.

- APRA administers the FCS, but it is only activated if the Treasurer declares an ADI to have failed — it is not a continuously running insurance product.

Other Australian depositor protection mechanisms

- Guarantee scheme for large deposits and wholesale funding

- Guaranteed deposit balances greater than $1 million and funding instruments with a maturity of 5 years or less

- Available to branches of foreign-owned banks

- Closed in March 2010 after the recovery of global funding conditions

- Financial Claims Scheme—Policyholders Compensation Facility

- Similar as FCS for DIs

- Available to general insurers authorised by APRA

Liquidity risk at other types of financial institutions

Optional reading

This chapter is optional reading. The mechanisms parallel those for DIs (forced asset sales, loss of confidence, run dynamics). Skim for context; not examinable in detail.

Life insurance companies

- Life insurance companies hold cash reserves and liquid assets to meet policy cancellations (surrenders) and working capital needs.

- Premium income and returns on investments usually cover policyholder surrenders, with government bonds serving as a liquidity buffer.

- If premium income is insufficient, insurers may sell liquid assets to meet demands.

- A loss of confidence in an insurer can lead to a run, with mass policy surrenders forcing asset liquidations at potentially low prices.

- Forced liquidations can push insurers towards insolvency, similar to banks (DIs).

Case study: Equitable Life

The Equitable Life Assurance Society — founded in 1762 and the world’s oldest mutual insurer — lost a 2000 House of Lords ruling (the Hyman case) on guaranteed annuity rates. The adverse ruling triggered a wave of policy surrenders, and the society closed to new business in December 2000. After an 18-year wind-down, its remaining policies were transferred to Utmost Life and Pensions on 1 January 2020, ending a 258-year history.

Property-casualty insurers

- Property–casualty (PC) insurers sell policies insuring against certain contingencies impacting either real property or individuals.

- Large unexpected claims may materialize and exceed the flow of premium income and income returns from assets.

- For example, natural disasters.

Finally…

Key takeaways

What to remember

- Liquidity ≠ solvency — but a liquidity shock can kill a solvent bank in 36 hours (SVB).

- Both sides of the balance sheet matter — deposit runs (liability side) often coincide with fire-sale losses on long-duration securities (asset side).

- Buffers come in two flavours — purchased (wholesale market) and stored (HQLA, central-bank reserves). Both have costs.

- Basel III gave us LCR and NSFR — short-term (30-day) and structural (1-year) liquidity ratios, both with a 100% minimum.

- Australia layers it on — APRA classifies ADIs as LCR (the Big 4 et al.) or MLH (smaller ADIs at 9%); 1 July 2025 brought mark-to-market and ELA-readiness tweaks.

- Safety nets create moral hazard — deposit insurance and the discount window protect the system but encourage risk-taking, which is why prudential rules are needed.

Suggested readings

- APRA Explains: Liquidity in banking.

- RBA: The Implementation of Monetary Policy: Domestic Market Operations.

- BIS: LCR - Liquidity Coverage Ratio.

- Prudential Standard APS 210 Liquidity.

- Acharya, V. V., Engle, R., Jager, M., & Steffen, S. (2024). Why Did Bank Stocks Crash during COVID-19? The Review of Financial Studies, 37, 2627–2684.

References

Acharya, Viral V, Robert Engle, Maximilian Jager, and Sascha Steffen. 2024. “Why Did Bank Stocks Crash During COVID-19?” The Review of Financial Studies 37 (9): 2627–84. https://doi.org/10.1093/rfs/hhae028.

AFIN8003 Banking and Financial Intermediation