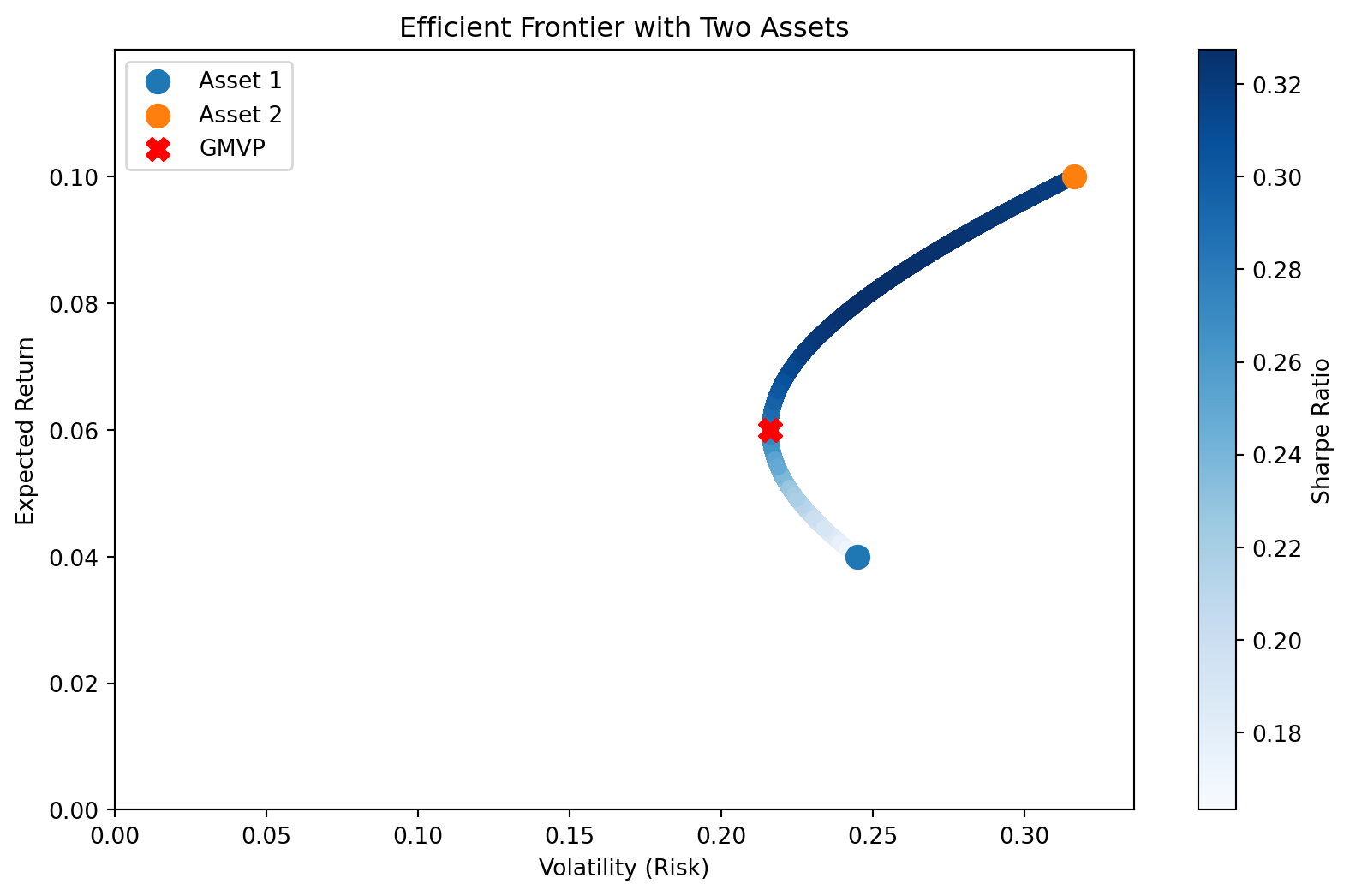

import numpy as np

import matplotlib.pyplot as plt

# Define annualized returns and covariance matrix for two assets

mean_returns = np.array([0.04, 0.1]) # Expected annual returns for two assets

cov_matrix = np.array([[0.06, 0.02], [0.02, 0.10]]) # Covariance matrix of returns

individual_volatility = np.sqrt(np.diag(cov_matrix)) # Volatility of individual assets

# Define the number of portfolios to simulate

num_portfolios = 10000

# Initialize empty lists to store portfolio returns, volatilities, and weights

results = np.zeros((3, num_portfolios))

# Simulate random portfolios

for i in range(num_portfolios):

# Generate random weights for the two assets

weights = np.random.random(2)

weights /= np.sum(weights) # Ensure weights sum to 1

# Calculate portfolio return and volatility (risk)

portfolio_return = np.dot(weights, mean_returns)

portfolio_volatility = np.sqrt(np.dot(weights.T, np.dot(cov_matrix, weights)))

# Store the results

results[0, i] = portfolio_volatility

results[1, i] = portfolio_return

results[2, i] = portfolio_return / portfolio_volatility # Sharpe ratio

# Calculate the Global Minimum Variance Portfolio (GMVP)

inv_cov_matrix = np.linalg.inv(cov_matrix)

ones = np.ones(len(mean_returns))

weights_gmvp = inv_cov_matrix.dot(ones) / ones.T.dot(inv_cov_matrix).dot(ones)

gmvp_return = weights_gmvp.dot(mean_returns)

gmvp_volatility = np.sqrt(weights_gmvp.T.dot(cov_matrix).dot(weights_gmvp))

# Plot the efficient frontier

plt.figure(figsize=(10, 6))

plt.scatter(

results[0, :], results[1, :], c=results[2, :], cmap="Blues", marker="o", alpha=1

)

plt.colorbar(label="Sharpe Ratio")

# Plot individual assets as red dots

plt.scatter(

individual_volatility[0],

mean_returns[0],

# color="red",

marker="o",

s=100,

label="Asset 1",

)

plt.scatter(

individual_volatility[1],

mean_returns[1],

# color="blue",

marker="o",

s=100,

label="Asset 2",

)

# Plot GMVP

plt.scatter(gmvp_volatility, gmvp_return, color="red", marker="X", s=100, label="GMVP")

# Set axis limits to start from 0

plt.xlim(0, np.max(results[0, :]) + 0.02) # Add a small margin on the right

plt.ylim(0, np.max(results[1, :]) + 0.02) # Add a small margin on the top

# Annotate the plot

plt.title("Efficient Frontier with Two Assets")

plt.xlabel("Volatility (Risk)")

plt.ylabel("Expected Return")

plt.legend(loc="upper left")

plt.show()