Understanding how capital safeguards a financial institution (FI) from insolvency risk requires a clear definition of capital. However, definitions vary significantly across different perspectives:

Economist’s Perspective: Economists define an FI’s capital, or owners’ equity, as the difference between the market values of its assets and liabilities, also known as net worth. This concept aligns with market value accounting.

Accounting Perspective: Accountants typically focus on book value, which is the historical cost of assets minus liabilities as recorded in financial statements.

Regulatory Perspective: Regulatory bodies have crafted definitions of capital that may diverge from economic net worth to prioritize financial stability. Regulatory capital requirements often rely on historical or book value accounting concepts.

Regulatory capital includes various tiers (e.g., Tier 1 and Tier 2) and is used to assess capital adequacy.

Capital of financial institutions (FIs)

The major functions of capital are

to absorb unanticipated losses to enable the FI to continue as a going-concern

to protect uninsured depositors, bondholders and creditors in case of insolvency and liquidation

to protect FI insurance funds and the taxpayer

to protect the FI owners against increases in insurance premiums

to partially fund the FI’s real investment activities

Why is capital important in a regulatory context? APRA’s explanation of capital

From a prudential regulator’s perspective, capital is a measure of the financial cushion available to an institution to absorb any unexpected losses it experiences in running its business. For a bank, such losses might include loans that default and are written off. Insurers might be hit by an unexpectedly high volume of claims in the wake of a major natural disaster.

Sufficient capital levels

inspire confidence in the FI

enable the FI to continue as a going concern even in difficult times

Capital and insolvency risk

Example of bank net worth (capital) absorbing losses

The marking-to-market method allows balance sheet values to reflect current rather than historic prices.

Consider the following market value balance sheet of an FI:

Table 1: Market-value-based balance sheet before loan losses

Assets ($m)

Amount

Liabilities ($m)

Amount

Securities

70

Deposits

85

Loans

30

Net worth

15

Total assets

100

Total liabilities + equity

100

In this example the FI is solvent on a market value basis.

Example of bank net worth (capital) absorbing losses

The marking-to-market method allows balance sheet values to reflect current rather than historic prices.

Consider a fall in the market value of loans to $10 (a fall of $20m).

Table 2: Market-value-based balance sheet after loan losses

Assets ($m)

Amount

Liabilities ($m)

Amount

Securities

70

Deposits

85

Loans

10

Net worth

-5

Total assets

80

Total liabilities + equity

80

FI is now insolvent, its net worth has declined from $15 to -$5. The owners’ net worth stake has been completely wiped out.

After the liquidation of the remaining $80 in assets, depositors would get only 80/85 in dollars, without deposit insurance.

The FI’s capital is used to absorb (partially) the losses.

The example also shows that market valuation of the balance sheet produces an economically accurate picture of the net worth and thus the solvency position of an FI.

The book value of capital

However, the FI’s balance sheet based on book value could remain unchanged.

Table 3: Book-value-based balance sheet after loan losses

With book value accounting, FIs have discretion in how and when they report loan losses on their balance sheets.

This flexibility allows them to strategically manage the recognition of these losses and their subsequent effect on capital.

For example, the FI could just record an increase in loan loss provisions to reflect their expected loan losses (e.g., $5m).

Table 4: Book-value-based balance sheet with loan loss provisions

Assets ($m)

Amount

Liabilities ($m)

Amount

Securities

70

Deposits

85

Loans

30

Net worth

10

less loan loss provisions

(5)

Total assets

95

Total liabilities + equity

95

Market-value vs book-value of equity

Obviously, market-value-based view of capital allows for a more accurate and comprehensive description of FIs’ financial health.

If regulators close a FI before it’s market value of capital reaches zero, liability holders will not lose.

But not all assets and liabilities are valued as fair value (market value).

Note

The Financial Accounting Standards Board (FASB) sets out Financial Accounting Standards (FAS) and the Generally Accepted Accounting Principles (GAAP), adopted in the U.S.

The International Accounting Standards Board (IASB) sets out the International Financial Reporting Standards (IFRS), adopted in many other places.

All trading assets, marketable securities (“available for sale”) are marked to market.

Loans and debt securities held for investment or to maturity are carried at amortized cost (book value).

Tip

Recall a bank’s banking book and trading book.

Why not market value for all?

Difficult to implement, especially for small banks, building societies and credit unions with large amounts of non-traded assets

Introduces unnecessary variability into an FI’s earnings

FIs are less willing to take long-term asset exposures such as commercial mortgages and business loans, since long-term assets are more interest rate sensitive.

Example balance sheet of a bank

Assets ($m)

Amount

Liabilities ($m)

Amount

Cash

20

Deposits

80

10-yr 5% corporate loans

100

Net worth

40

Total assets

120

Total liabilities + equity

120

Change in market conditions (like yield) can cause significant variation in bank’s capital value.

Code

viewof cash = Inputs.range( [0,100], {value:20,step:1,label:"Cash:"})viewof capital = Inputs.range( [0,100], {value:40,step:1,label:"Initial capital:"})d = {const c =0.05, m =10;const loan =100;const y =0.05;functionpv(c, f, t, r) {return c * (1- (1+r)**(-t)) / r + f / (1+r)**(t) }const prices = {"YTM": [],"Equity": []};let coupon = loan * c;let deposits =120- capital;for (let ytm =0.01; ytm <20; ytm++) {let mvloan =pv(coupon, loan, m, ytm/100);let dy = ytm - y*100; prices["YTM"].push(dy); prices["Equity"].push(cash + mvloan - deposits); }return prices;}Plot.plot({caption:"Assume current YTM of 5%.",x: {padding:0.4,label:"Change in YTM (%)"},grid:true,marks: [ Plot.ruleY([0]), Plot.ruleX([0]), Plot.lineY(transpose(d), {x:"YTM",y:"Equity",stroke:"blue"}), ]})

As a result, market value accounting may interfere with FIs’ special functions as lenders and monitors and may even result in (or accentuate) a major credit crunch.

Capital management and regulation

In summary,

capital is useful to absorb losses and to mitigate insolvency risk;

regulators use book value accounting standards to determine the adequate capital requirements for FIs.

As a result, FI’s capital is guided by two key factors:

regulated capital adequacy requirements, and

the risk-return trade-offs.

Risk-based capital ratio

Who determines the capital requirements?

Actual capital ratios applied can be country-specific, determined by national regulators. However, the Basel Accords provide the global framework for these capital ratios.

The Basel Committee on Banking Supervision (BCBS) of the BIS sets out the 1988 Basel Capital Accord.

Member countries of the BIS agreed and implemented the Basel Capital Accord (Basel I).

a minimum ratio of capital to risk-weighted assets of 8%.

A series of updates led to the Basel Accord of 2006 (Basel II)

Basel III: responding to the 2007-09 financial crisis.

Basel I

Two capital ratios:

Tier 1 Capital Ratio

Primarily composed of common equity, retained earnings, and disclosed reserves, less goodwill and other intangibles.

Calculation: Tier 1 Capital / Risk-Weighted Assets (RWA)

Minimum requirement: 4%

Total Capital Ratio

Minimum requirement: 8%

Features:

Basel I introduced the systematic measurement of capital adequacy through the use of risk-weighted assets.

Basel I utilized RWA to account for the varying risk levels of different asset classes, including both on-balance-sheet and off-balance-sheet exposures.

Criticisms:

Credit Risk Focus: Basel I primarily recognized credit risk in the calculation of risk-weighted assets. It did not initially incorporate market risk or operational risk, leading to criticisms that it did not fully address the spectrum of risks faced by banks.1

Basel II

Basel II comprised three pillars:

minimum capital requirements, which sought to develop and expand the standardised rules set out in the 1988 Accord

supervisory review of an institution’s capital adequacy and internal assessment process

effective use of disclosure as a lever to strengthen market discipline and encourage sound banking practices

The measurement of capital did not change markedly in Basel II.

The measurement of risk was significantly enhanced to include operational risk, some market risks in the banking book, and risks associated with securitisation.

Under Basel II, two options are allowed for banks to measure their credit risk:

Standardized approach. Similar to Basel I, but more risk-sensitive.

Internal ratings-based (IRB) approach. Banks can use their internal rating system or credit scoring models to assess their portfolios, subject to regulatory approval.

Three options are available for measuring operational risk:

basic indicator.

standardized approach.

advanced measurement approach.

GFC and Basel 2.5

The Global Financial Crisis (GFC) in 2007-09 revealed that Basel II was flawed. For example,

credit ratings of complex securities were conducted by private companies without regulatory supervision or review

Basel II capital adequacy formula was procyclical, meaning that the required capital was increasing as the crisis unfolded, making it even harder for banks during crisis

In response, Basel 2.5 was passed in 2009 (effective in 2013) and Basel III was passed in 2010 (phased in between 2013 and 2019).1

Basel 2.5 updated capital requirements on market risk from banks’ trading activities.

Basel III

Basel III is broader in perspective than just a revision of capital, capital adequacy, risk measurement and supervision. It introduced macroprudential measures, targeting the protection of the whole financial system.

Three pillars similar to in Basel II, but with significant enhancements.

Improvements to both standardized and IRB approaches in calculating adequate capital.

Inclusion of new capital conversion buffer and countercyclical capital buffer to the minimum required capital level.

Introduction of two minimum standards for funding liquidity: liquidity coverage ratio and net stable funding ratio.1

Higher capital requirements for trading and derivative activities.

Enhanced bank governance.

Enhanced risk disclosure.

Note

Basel III is our focus, of course.

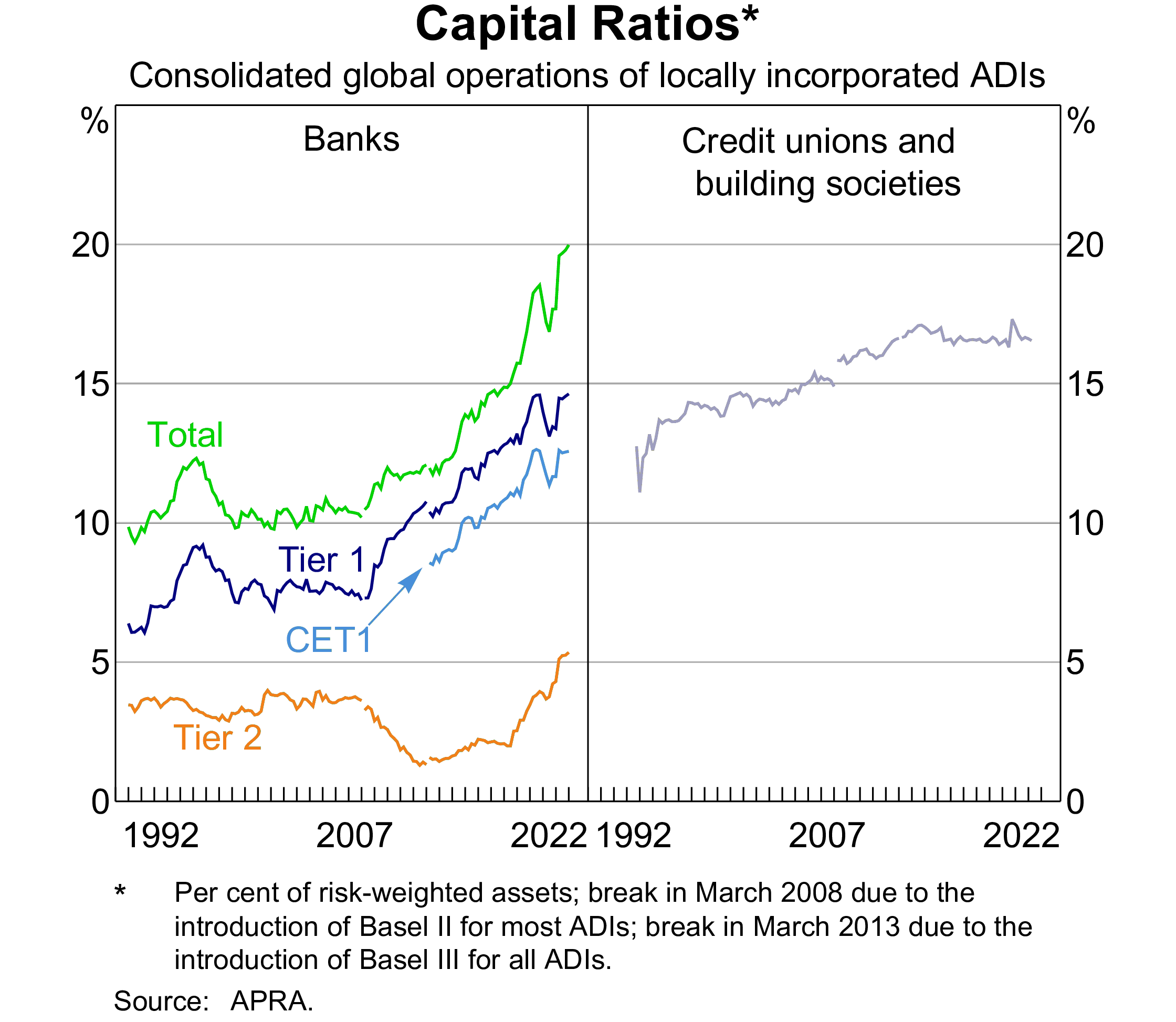

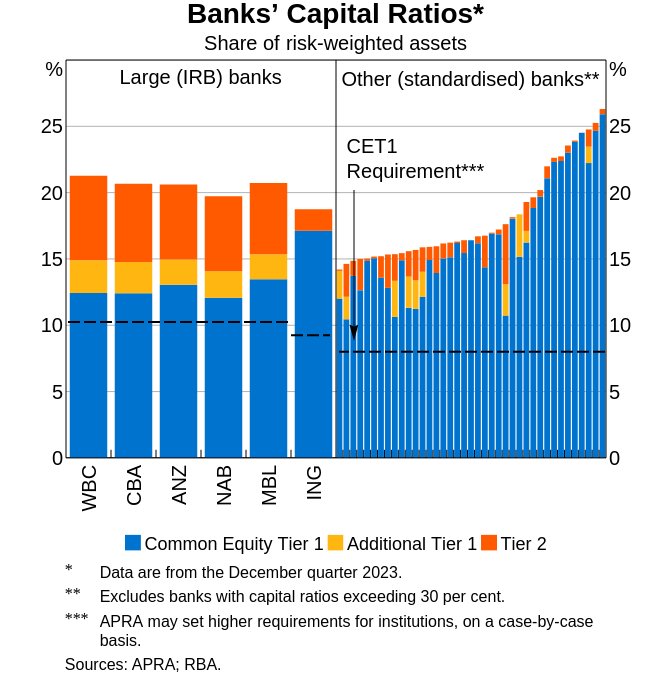

Risk-based capital ratio

Under Basel III, depositary institutions (DIs) calculate and monitor four capital ratios:

Common equity Tier 1 (CET1) risk-based capital ratio\[

\text{CET1 capital ratio} = \frac{\text{CET1 capital}}{\text{Risk-weighted assets}}

\tag{1}\]

Tier 1 risk-based capital ratio\[

\text{Tier 1 capital ratio} = \frac{\text{Tier 1 capital}}{\text{Risk-weighted assets}}

\tag{2}\]

Total risk-based capital ratio\[

\text{Total capital ratio} = \frac{\text{Total capital}}{\text{Risk-weighted assets}}

\tag{3}\]

Total exposure is equal to the DI’s total assets plus off-balance-sheet exposure.

For derivative securities, off-balance-sheet exposure is current exposure plus potential future exposure as described earlier.

For off-balance-sheet credit (loan) commitments, a conversion factor of 100 percent is applied unless the commitments are immediately cancelable.

Risk-based capital: beyond credit risk

So far, the capital ratios (specifically, RWA) are calculated to account for the DI’s credit risk. However, a DI’s insolvency risk can also manifest from interest rate risk, market risk, operational risk, and more.

In Basel III, RWA should be the sum of three components:1

RWA for credit risk (covered in this lecture)

RWA for market risk. Can be calculated using two approaches:2

Standardized approach proposed by regulators. Revised standards published in 2016 to be implemented in 2019.

DI’s internal market risk model subject to regulator approval. Move towards expected shortfall rather than value at risk (VaR).

RWA for operational risk. Some complicated calculation.3

Important

The RWA in the minimum capital ratios (Equation 5) is the sum of all three RWAs.

We covered only the RWA for credit risk.

Risk-based capital: beyond credit risk

In the previous example, we have calculated that the DI’s RWA (for credit risk) is $97.4 million.

Now, suppose that we have also calculated that the DI’s

RWA for market risk is $10.2 million, and

RWA for operational risk is $9 million.

The total RWA is $97.4 + $10.2 + $9 = $116.6 million.